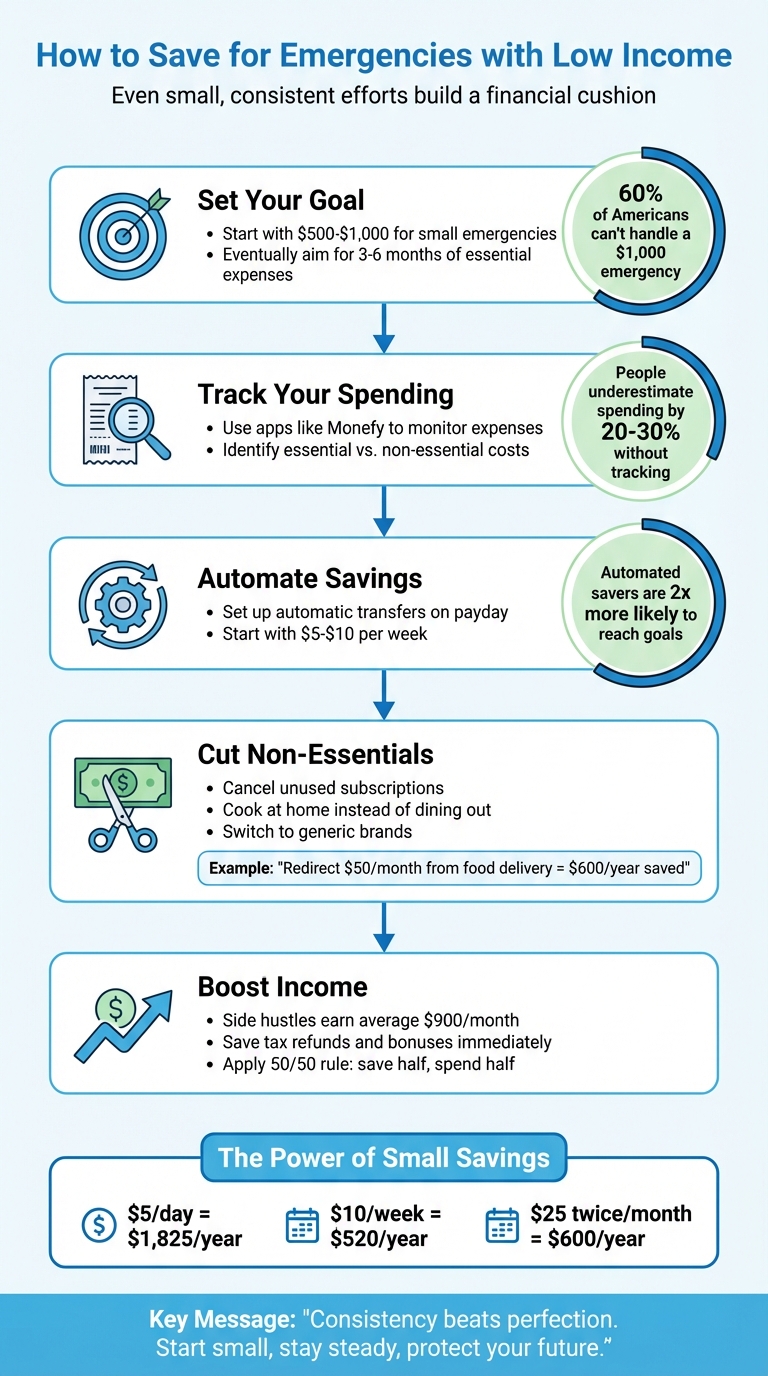

Saving for emergencies on a tight budget can feel challenging, but it’s not impossible. Even small, consistent efforts can build a financial cushion over time. Here’s how you can start:

- Set a realistic goal: Start with $500–$1,000 for smaller emergencies. Eventually, aim for 3–6 months of essential expenses.

- Track your spending: Use tools like Monefy to identify where your money goes and find areas to cut back.

- Automate savings: Schedule automatic transfers to a separate high-yield savings account to build your fund without extra effort.

- Cut non-essential costs: Reduce spending on subscriptions, dining out, and other discretionary expenses.

- Boost income: Take on side gigs or save windfalls like tax refunds to grow your fund faster.

Even saving $5 a day adds up to $1,825 in a year. Building an emergency fund is about consistency, not perfection. Start small, stay steady, and protect yourself from unexpected financial stress.

5-Step Emergency Fund Savings Plan for Low Income Earners

Calculate Your Emergency Fund Goal

When planning your emergency fund, focus on covering essential expenses rather than your entire income. The idea is to calculate what you’d need to stay afloat if your paycheck suddenly stopped.

Assess Your Essential Monthly Expenses

Start by reviewing your bank and credit card statements from the past 3–6 months. Look for the must-have expenses that keep your household running, often found in your bank account history. These include:

- Housing: Rent or mortgage payments.

- Utilities: Electricity, water, heating.

- Food: Basic groceries and toiletries.

- Transportation: Gas, insurance, or public transit costs.

- Healthcare: Medications and necessary treatments.

- Debt Payments: Minimum payments on loans or credit cards.

- Occasional Essentials: Annual costs like car registration or insurance premiums.

This isn’t about maintaining your usual lifestyle - it’s about creating a bare-bones survival budget. For example, if your essential spending was $2,800 in January, $3,300 in February, and $2,900 in March, your average monthly expense would be $3,000.

Here’s a quick breakdown of what to include and exclude:

| Expense Category | Include in Calculation | Exclude from Calculation |

|---|---|---|

| Housing | Rent, mortgage, property taxes | Home decor, renovations |

| Food | Groceries, basic toiletries | Dining out, specialty coffee |

| Utilities | Power, water, heat, basic phone/internet | Premium cable, high-speed gaming tiers |

| Transportation | Gas, insurance, public transit, registration | Car detailing, non-essential travel |

| Financial | Minimum loan/credit card payments | Extra principal payments, new investments |

Once you’ve calculated your average monthly essential expenses, you’ll have a clear foundation for setting your savings goal.

Set a Realistic Savings Target

Research shows that nearly 60% of Americans can’t handle a $1,000 emergency using their savings. Starting small - between $500 and $1,000 - can help you manage unexpected costs like a flat tire, minor medical bills, or urgent home repairs. As Evelyn Waugh, Personal Finance Writer at Experian, puts it:

"Aiming to put $1,000 or even $500 in emergency savings can be a solid starting point".

Once you hit that initial target, aim for a full emergency fund covering three to six months of essential expenses. Using the $3,000 monthly example, this would mean saving between $9,000 and $18,000. If you’re self-employed, a contractor, or the sole income earner, consider building a cushion of nine to twelve months of expenses.

The key is consistency, not speed. For instance, saving $166.67 per month could get you to $10,000 in five years, while saving $333.33 per month would cut that time in half to about 2.5 years. Find a pace that works with your budget, and adjust as your income or expenses change. Even small, steady contributions can make a big difference over time.

sbb-itb-02fd20a

Track Expenses with Monefy to Find Savings Opportunities

Understanding your spending habits is a crucial step in building an emergency fund. Before you can start saving, you need a clear picture of where your money is going. Studies show that most people underestimate their spending by 20% to 30% when relying on memory rather than actual data. This is where tracking every dollar becomes vital, and Monefy makes the process simple and engaging.

Monitor Spending Categories

Monefy uses a visual interface with circles and charts, giving you an easy way to see where your money goes each month. Because the app requires you to manually enter transactions, it keeps you actively involved in understanding your spending habits. Whether it’s a $4.50 coffee or a $65 grocery trip, logging each expense helps you stay mindful of your financial patterns.

To get started, create spending categories that reflect your actual habits. For example, instead of grouping all food expenses together, separate "Takeout" from "Groceries" to better understand how much you're spending on convenience versus essentials. Include categories for necessities like housing, utilities, transportation, healthcare, and debt payments - these align with the core expenses you calculated for your emergency fund. Add discretionary categories like dining out, subscriptions, coffee shops, and entertainment to capture non-essential spending.

Make it a habit to log every transaction within 24 hours for at least two months. This will give you a reliable baseline for your spending. Add short notes when needed to identify patterns, like frequent impulse buys or recurring charges. Monefy also lets you track multiple accounts separately, such as checking, savings, and cash. This feature is especially useful for monitoring money transfers into your emergency fund without accidentally double-counting expenses.

Once you’ve mapped out your spending, you can start identifying areas to trim.

Spot Areas to Cut Back

After two months of tracking, review your data to find opportunities to reduce non-essential spending and redirect those savings to your emergency fund. The app’s visual breakdown makes it easy to see when spending on "wants" is overshadowing "needs". Look for trends in categories like subscriptions, dining out, or impulse purchases where small adjustments could make a big difference.

Here’s a quick guide to help you evaluate your spending:

| Category Type | What to Look For | Potential Action |

|---|---|---|

| Discretionary | Dining out, coffee shops, streaming services | Cook meals at home; cancel unused subscriptions |

| Variable Essentials | Groceries, utilities, transportation | Opt for generic brands; conserve energy; carpool |

| Financial Fees | ATM fees, overdrafts, bank charges | Use in-network ATMs; switch to fee-free accounts |

When you identify an expense to cut - like a $12.99 subscription you rarely use - transfer that exact amount to your emergency fund right away and log it in Monefy. This "found money" strategy helps you see immediate progress. Check your Monefy balance weekly to stay on track and make adjustments before small oversights snowball into bigger issues. For guidance, you can follow the 50/30/20 rule: allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

Set Up a Dedicated Savings Account

Now that you've identified ways to save, it's time to secure those funds in a dedicated account meant only for emergencies. Keeping your emergency savings in the same account as your regular spending money can lead to accidental splurges. By separating these funds, you create a clear boundary that helps protect your financial safety net.

A separate account acts like a safeguard against dipping into your emergency fund for non-essential purchases. As Navy Federal Credit Union explains:

"Using just one account may make it far too easy to 'borrow' from your emergency fund for non-essential items".

When emergency funds sit in your checking account, they feel too accessible - and that's where the trouble begins. Surprisingly, about 29% of people stash their emergency savings in cash at home. While this may seem convenient, it exposes the money to risks like theft, natural disasters, and, unfortunately, zero interest growth.

Choose a High-Yield Savings Account

A high-yield savings account (HYSA) is a smart choice for storing your emergency fund. These accounts offer much higher interest rates than standard savings accounts, allowing your money to grow while remaining accessible when you need it. Many banks and credit unions provide HYSAs with minimal or no initial deposit requirements.

When choosing an account, prioritize features like FDIC insurance (which covers up to $250,000 per depositor), no monthly maintenance fees, and seamless electronic transfers. It's also a good idea to avoid certificates of deposit (CDs) for emergency savings - they lock your money away for a set period and charge penalties for early withdrawals. To further discourage impulsive spending, consider opening the account at a different bank than where you manage your everyday checking. This extra layer of separation helps ensure the money stays untouched until a genuine emergency arises.

Name the Account for Motivation

Naming your savings account can give it a sense of purpose and keep you motivated. Something like "Emergency Fund Only" or "Safety Net" serves as a constant reminder of the account's role in your financial plan. Every time you check your balance, the name reinforces that these funds are strictly for emergencies.

If your bank allows it, you can even create multiple subaccounts with different labels. For instance, one could be "Emergency Fund" for major crises like job loss, while another, "Rainy Day Fund", could cover smaller but inevitable expenses like car repairs. With only 41% of Americans feeling confident about their emergency savings, this simple naming strategy can help you stay focused on your goals. Seeing "Emergency Fund: $327.50" instead of just "Savings" provides a clear visual of your progress and reminds you of the security you’re building. A well-labeled account is a small but effective step toward maintaining a reliable financial cushion.

Automate Small, Consistent Transfers

Once you’ve set up your dedicated savings account, the next step is to make deposits automatic. Why? Because automation takes the decision-making out of the process, ensuring your emergency fund grows steadily without needing constant attention. As Amy Miller, an Accredited Financial Counselor at America Saves, explains:

"Automatic savings is a simple yet powerful tool that ensures you're consistently working toward your financial goals... it removes the need to think about payments every month".

Studies show that people who automate their savings are nearly twice as likely to hit their financial targets. The logic is straightforward - when the money is transferred automatically, it’s out of sight and out of mind, making it less likely to be spent on unnecessary expenses. This "set it and forget it" approach turns saving into a priority without extra effort.

There are a few ways to automate your savings:

- Split your direct deposit: Ask your employer to send a portion of your paycheck directly into your savings account.

- Set up recurring transfers: Schedule automatic transfers from your checking account to your savings on a specific day each month.

- Use round-up programs: Some banks offer tools that round up your debit card purchases to the nearest dollar and transfer the spare change into your savings (e.g., $0.55 from an $87.45 purchase).

To make saving even easier, schedule these transfers on payday so you’re essentially “paying yourself first.”

Start with Micro-Savings

If your budget feels tight, start small. Even saving $5–$10 a week can help you build the habit without stretching your finances too thin. George Morris from InCharge Debt Solutions sums it up perfectly:

"Money that is automatically transferred from your paycheck to your savings account is money you don't miss".

Most people find they naturally adjust their spending when their checking account balance is slightly lower.

Here’s how small, consistent transfers can add up over a year:

| Savings Amount | Frequency | Annual Total (Before Interest) |

|---|---|---|

| $10 | Weekly | $520 |

| $20 | Bi-weekly | $520 |

| $25 | Twice Monthly | $600 |

| $50 | Monthly | $600 |

Even $10 a week adds up to $520 a year. If you can save $25 twice a month, you’ll have $600 in just 12 months. And if you’re using a high-yield savings account, the interest earned will help your fund grow even faster.

To avoid overdraft fees, keep a close eye on your account balance or set up bank alerts. If your income varies, adjust your automated transfers during lean weeks and add extra funds manually when you’re able. The Consumer Financial Protection Bureau offers this advice:

"Saving automatically is one of the easiest and most effective ways to get started with a new savings habit. Consistently putting money aside - even in small amounts - will add up over time".

Increase Contributions Over Time

Once you’ve built the habit, gradually increase your contributions as your financial situation improves. Got a raise or a bonus? Use it as an opportunity to boost your automated savings. Review your settings every few months to see if you can bump up the amount. For example, if you started with $10 per week, try increasing it to $15 or $20. Similarly, if you’re saving $25 twice a month, consider raising it to $30 or $35.

These small adjustments can make a big difference over time. The best part? Once you update your automation settings, the higher amount becomes your new baseline - no extra effort required.

Cut Non-Essential Spending

Once you’ve set up automated savings, the next step is to redirect extra funds from non-essential expenses into your emergency fund. Many people don’t realize how much room they have in their budget until they take a closer look at where their money is going. As of February 2024, about 66.2% of Americans reported living paycheck to paycheck, making every dollar matter. Even trimming small amounts from non-essential spending can free up extra cash to grow your savings.

Take a close look at your recent statements to identify recurring charges or daily habits that quietly drain your budget.

Evaluate Subscription Services

Subscriptions are often one of the easiest areas to cut back on. Streaming platforms like Netflix, HBO, Disney+, and Hulu, along with music services and gym memberships, are common culprits. Many people pay for multiple subscriptions they barely use simply because the charges are automatic and easy to forget.

Go through your statements and ask yourself: Do I actually use this? If you haven’t used a service in a while, cancel it. If you’re not ready to give it up entirely, consider switching to a lower-cost, ad-supported plan instead of a premium one.

For services like cable, internet, or cell phone plans, it’s worth calling your provider to ask about promotional rates or loyalty discounts. Luke Crumbaker, Program Manager at Greenville County Financial Empowerment Centers, suggests:

"If you have an annual contract for cable or internet, you can typically get a newer promo rate even if you're an existing customer".

Adopt Budget-Friendly Habits

Beyond subscriptions, everyday spending habits can also offer opportunities to save. Small, frequent expenses like takeout meals, dining out, or daily coffee runs can add up quickly, especially if you’re on a tight budget. The goal isn’t to cut out everything you enjoy but to find more cost-effective ways to maintain your lifestyle.

Cooking at home is one of the best ways to save. Plan meals around weekly grocery sales and focus on affordable staples like eggs, beans, and chicken instead of pricier proteins. Setting aside one evening a week to batch-cook basics like rice, beans, or roasted meats can save you from costly workday lunches or last-minute takeout.

Food delivery services are another big expense for many households. Redirecting just $50 a month from these services can make a noticeable difference in your savings over time.

Transportation is another area to evaluate. Walking, biking, or using public transit can save on gas and reduce wear-and-tear on your car. If driving is unavoidable, use apps to find the cheapest gas prices and keep up with maintenance to improve fuel efficiency. For families with multiple vehicles, consider whether you could manage with just one.

Switching to generic brands for groceries, medications, and toiletries is another simple way to cut costs. Public libraries are also a great resource for borrowing movies, music, and books instead of buying them. Many libraries even offer free digital lending for e-books and audiobooks.

For larger savings, explore local "Buy Nothing" groups or platforms like Freecycle to find furniture, clothing, and household items for free. You could also try a no-spend weekend or month, where you limit spending to essentials like rent and basic groceries. This can help reset your spending habits and give your savings a boost.

Boost Savings with Side Income and Windfalls

Bringing in extra income through side gigs or unexpected financial windfalls can help you grow your emergency fund faster without sacrificing essentials. For those on a tight budget, earning more is just as critical as trimming expenses. Consider this: over 11 million people in the U.S. take on gig jobs or side hustles to supplement their main income. On average, these side hustlers earn close to $900 a month, which can make a big difference when you're trying to build a financial safety net.

Take Advantage of Side Hustles

Side gigs don’t have to take over your life. Plenty of flexible options exist that require little to no upfront investment and can fit into your current schedule. For example, pet sitting, house cleaning, yard work, or grocery delivery are easy-to-start options that can pay anywhere from $10 to $75 an hour, depending on the task. If you have specialized skills - like tutoring, graphic design, or virtual assistance - you can command even higher rates.

For smaller, more incremental boosts, micro-tasks like online surveys or website testing are worth considering. Website testers, for instance, often earn about $10 for a 15–20 minute session, while participating in focus groups can bring in $50 to $200 per session.

You can also make money using what you already own. For instance, Airbnb hosts typically earn over $13,800 annually, while car-sharing platforms like Turo bring in an average of $10,516 per vehicle per year. Even renting out unused spaces like a parking spot, garage, or basement can provide steady passive income.

Dennis Shirshikov, a Finance Professor at the City University of New York, recommends aligning your side hustle with your current job:

"Aligning your side hustle with your full-time job can be highly beneficial because it allows you to leverage your existing skills and industry knowledge".

He also emphasizes the importance of balance:

"Allow yourself downtime to recharge; neglecting self-care can quickly lead to burnout. Remember, the goal is to enhance your life, not overwhelm it".

To avoid feeling overwhelmed, start with just one or two side gigs that work well with your schedule. Be sure to set aside 25–30% of your side income for taxes, and direct the rest toward your emergency savings.

Unexpected financial gains can also give your savings a much-needed boost.

Save Bonuses and Tax Refunds

Unexpected income - like tax refunds, work bonuses, cash gifts, or insurance payouts - can be a game-changer for building or replenishing your emergency fund. For many Americans, a tax refund is the largest single check they receive in a year.

The trick is to allocate these windfalls immediately to your savings before they get absorbed into everyday expenses. To make this easier, you can arrange for tax refunds or bonuses to be direct-deposited into your savings account instead of your checking account.

As Vanguard research points out:

"By putting it in a separate account, you'll know exactly how much you have - and how much you may still need to save. And you'll be less inclined to tap into it before the need arises".

If you’re tempted to spend the extra cash, try the 50/50 rule: save at least half for emergencies and use the rest for immediate needs or small indulgences. Windfalls can also help you hit smaller savings milestones, like reaching $500 or $1,000, which can motivate you to keep going. Studies show that having even $2,000 in an emergency fund can greatly improve financial well-being - just as much as having $1,000,000 in total assets.

Maintain and Grow Your Emergency Fund

Once you've established your emergency fund, the next step is ensuring it stays intact for when you truly need it. Without clear boundaries, it’s easy to dip into these savings for non-urgent expenses, leaving you unprepared when a real crisis arises.

Use the Fund Only for True Emergencies

Not every surprise expense qualifies as an emergency. Before tapping into your fund, ask yourself: Is this expense unexpected, necessary, and urgent? If it doesn’t check all three boxes, it’s probably not a true emergency.

Certified Financial Planner Matt Stephens underscores the importance of this discipline:

"Emergency funds are incredibly important because it keeps people from running up credit card debt or pulling money out of retirement accounts to pay for things, both of which can be devastating to your finances".

To help resist temptation, consider naming your account something like "Safety Net" or "Emergency Only." This simple step can act as a mental barrier to casual withdrawals. Non-emergency expenses - like a new gadget or a vacation - should come from separate savings.

For example, a broken dishwasher might be inconvenient, but if you can manage by handwashing dishes temporarily, it’s not an emergency. On the other hand, a leaky roof or failed brakes on your car qualifies because they carry safety risks or could lead to bigger problems.

If you do need to use the fund, make it your top priority to replenish it as soon as possible.

Replenish the Fund After Use

Once an emergency depletes your fund, rebuilding it should be a financial priority. Financial coach Netta Stahl highlights the importance of a focused approach:

"Rebuilding requires intentional budgeting... sticking with old spending patterns while trying to replenish the fund will only slow progress".

Start by setting up automatic monthly transfers from your checking account to your emergency fund. Additionally, direct any unexpected income - like tax refunds, bonuses, or gifts - toward rebuilding. For many, it takes about a year of concentrated effort to fully restore a six-month emergency fund.

If cash flow is tight, consider temporarily reallocating money from other savings goals, such as vacations or down payments, to speed up the process. You can also contact your creditors to explore hardship programs that might reduce payments or waive fees, freeing up extra funds to rebuild your safety net.

Conclusion

Building an emergency fund on a low income is possible with steady, manageable steps. Even small contributions, like $5 a day, can add up to $1,825 over a year. The trick is to treat your savings like a fixed monthly expense - something non-negotiable, regardless of how tight your budget feels.

Start with a realistic goal, such as saving $500 to $1,000. Studies show that even having less than one month’s income saved can significantly reduce the risk of falling behind on bills or resorting to high-interest loans compared to having no savings at all.

As Bank of America wisely advises:

"Any emergency savings is better than none. What's important is that you're saving, reducing the chance that you'll have to take on debt in an emergency".

Automating your savings is a game-changer. Set up recurring transfers and direct unexpected windfalls - like tax refunds or bonuses - straight into your fund. Tools like Monefy can help you track spending and spot extra money to save.

FAQs

What counts as a real emergency?

Unexpected expenses can strike when you least expect them, and they often demand immediate action. Think about situations like sudden medical bills, urgent car repairs, storm damage to your home, or expenses tied to the illness or loss of a loved one. These aren’t the kinds of costs you can delay - they’re pressing and often unavoidable. That’s why having money set aside for emergencies is so important.

How do I save if I’m living paycheck to paycheck?

Saving money while living paycheck to paycheck can feel tough, but it’s definitely possible with a bit of planning and consistency. Begin by taking a close look at your spending habits to spot areas where you can trim costs. Set specific goals, like creating an emergency fund, to give your savings a clear purpose.

One effective strategy is to automate your savings - schedule small, regular transfers into a savings account. Even tiny amounts can add up over time, giving you a safety net for unexpected expenses and helping you work toward greater financial security.

Where should I keep my emergency fund?

When it comes to your emergency fund, the smartest choice is to keep it in a place that's both low-risk and easily accessible. Options like a high-yield savings account, a money market account, or certificates of deposit (CDs) fit the bill perfectly. These choices not only keep your money safe but also let it earn some interest.

What you want to avoid? Stashing it under your mattress or in accounts that come with high fees or restrictions. These could make it harder - and slower - to access your cash when you need it most.