When your income increases, it’s easy to fall into the trap of lifestyle inflation - spending more just because you’re earning more. This can leave you financially stuck, even with a higher paycheck. To avoid this, focus on strategies that help you save, invest, and spend intentionally. Here’s a quick overview of 10 actionable ways to prevent lifestyle inflation:

- Automate Savings: Set up automatic transfers to savings or investment accounts.

- Track Spending: Use tools like Monefy to monitor expenses and identify spending leaks.

- Set Financial Goals: Break them into short, medium, and long-term targets.

- Avoid Upgrades: Stick with your current home or car to avoid unnecessary costs.

- Make Intentional Purchases: Pause and evaluate before buying non-essential items.

- Resist Social Pressure: Set boundaries and suggest budget-friendly activities.

- Review Fixed Expenses: Regularly audit subscriptions, insurance, and other recurring costs.

- Build an Emergency Fund: Save 3–6 months of essential expenses to handle unexpected costs.

- Separate Needs from Wants: Prioritize necessities and limit spending on luxuries.

- Use Accountability Tools: Leverage budgeting apps or trusted partners to stay on track.

10 Strategies to Prevent Lifestyle Inflation and Build Wealth

1. Set Up Automatic Savings Transfers

A great way to sidestep lifestyle inflation is by automating your savings. Setting up recurring transfers from your checking account to your savings or investment accounts takes the guesswork out of saving. This ensures your money is allocated before you're tempted to spend it on things like a pricier car, a bigger apartment, or daily coffee splurges.

This approach follows the "pay yourself first" rule, treating savings as a priority rather than an afterthought. To make it seamless, schedule your automatic transfers for the same day your paycheck hits. That way, your savings grow before you even have the chance to consider spending the money elsewhere.

If you're just starting, begin with a manageable amount. Even $25 a week or $50 a month can help you build the habit. While many experts suggest saving 10% to 20% of your take-home pay, the key is consistency. You can always increase the amount over time.

When your income rises, adjust your savings transfer by 1–2% to stay on track with your goals. This ensures that any extra income benefits your future instead of fueling unnecessary spending. Some employers even offer the option to split your direct deposit, sending part of your paycheck directly into a savings account - making it even easier to save without thinking about it.

The power of compounding can make a big difference over time. For example, saving $50 every two weeks instead of $1,300 once a year could result in an extra $6,024 after 30 years at a 5% return, thanks to more frequent compounding. As Michael Ryan, retired financial planner and founder of MichaelRyanMoney.com, explains:

"Automation is the cure for a lack of willpower. You will never have to decide between saving and spending if the saving has already happened."

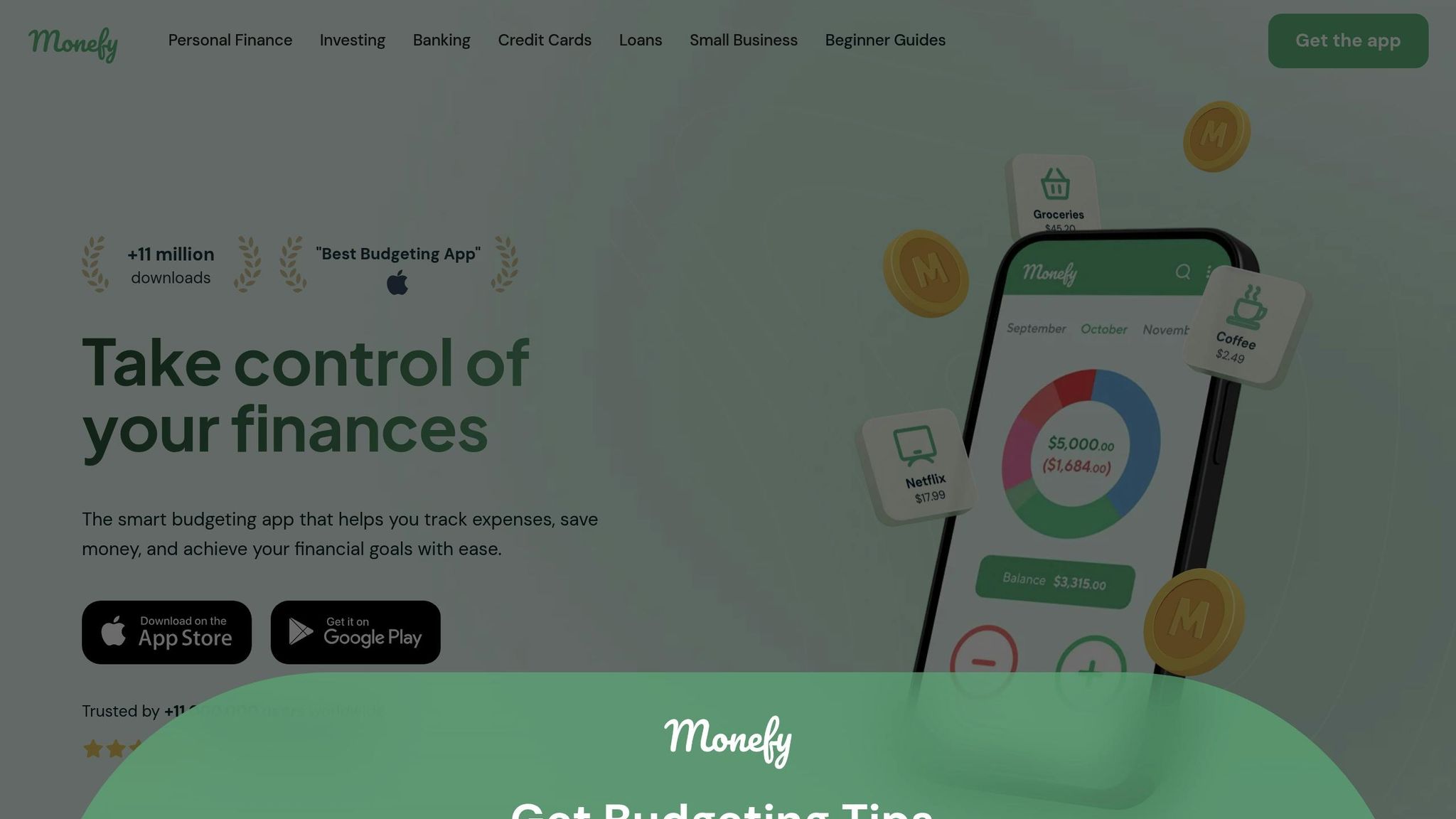

2. Track Your Spending with Monefy

Keeping tabs on every expense is key to managing your finances effectively. Studies show that people tend to underestimate their spending by 20% to 30% when relying on memory instead of a tracking tool. This is where Monefy steps in, offering a clear view of your finances with visual charts and real-time tracking. It shines a spotlight on spending leaks, helping you address them before they spiral into lifestyle inflation.

Monefy uses manual entry, which keeps you actively involved in tracking your expenses. This hands-on method can cut your spending by up to 25% in just the first month. While automated tools sync directly with your bank, Monefy’s approach builds a deeper awareness of where your money is going, making it easier to resist impulse purchases. As Monefy points out:

"The first step to stopping overspending is making your money visible. You can't fix what you can't see".

The app allows you to customize 8 to 12 categories, helping you uncover hidden costs. For example, you can separate "Takeout" from "Groceries" or track "Coffee Shops" as its own category. This level of detail helps you identify where small expenses add up, enabling you to redirect that money toward savings. The visual interface also provides a quick snapshot of your spending patterns, showing when discretionary spending (like dining out or shopping) starts to outweigh essential expenses (like rent or utilities).

Monefy also lets you manage multiple accounts - checking, savings, credit cards, and even cash - all in one place. This makes it easier to monitor your overall cash flow and avoid overspending on credit while neglecting other accounts. Transactions can be logged in just seconds, and a quick 10-minute review of your data each Sunday can help you spot overspending triggers before they turn into habits.

3. Set Clear Financial Goals

Without clear goals, extra income tends to disappear. Financial goals give you a solid reason to save, transforming what might feel like a restrictive budget into a plan for building wealth. For example, setting goals like saving for a down payment or maxing out your 401(k) can help curb the temptation to spend impulsively.

Break your goals into three categories: short-term (under a year), medium-term (1–5 years), and long-term (5+ years). In the short term, focus on paying off high-interest debt, like credit cards, which can drain your finances over time. Medium-term goals might include saving for a big purchase, such as a home or a child’s education. For the long term, think about contributing to retirement accounts or creating passive income streams.

A great way to structure your goals is by using the SMART framework: make them Specific, Measurable, Achievable, Relevant, and Time-bound. For instance, instead of vaguely deciding to "save more", aim for something like "save $1,000 in three months by setting aside $80 per week". You can also apply the 50/15/5 rule: allocate 50% of your take-home pay to necessities, 15% of your pre-tax income to retirement savings, and 5% to short-term savings. By sticking to such specific targets, you ensure your extra income is put to work growing your wealth rather than funding unnecessary lifestyle upgrades.

Having clear goals helps you make better spending choices. As Fidelity explains:

"It's not about how much you earn, but how wisely you manage your money that determines your financial future".

When you know what you're working toward, every dollar saved becomes a step closer to achieving something meaningful.

4. Avoid Upgrading Your Home or Car

Housing and transportation account for about 50% of the average American household's spending. These aren’t short-term expenses you can easily adjust, like cutting back on dining out or canceling a subscription. Once you commit to a bigger home or a fancier car, you’re locking yourself into costs that are tough - and expensive - to undo.

The real issue isn’t just the upfront cost. Upgrading your home or car comes with a ripple effect of added expenses: higher insurance premiums, increased property taxes, steeper maintenance costs, and additional fees like registration. As Daniel May, CFP®, explains:

"When you 'upgrade' in life, you're not only paying the (higher) base price for something, you're also paying for all the additional stuff that comes with it."

Here’s a striking example: a 2024 BMW M4 with a $78,000 price tag is projected to lose about $31,200 in value over five years - a 40% depreciation. Now imagine putting an extra $30,000 a year into investments instead. At a 6% annual return, that money could grow to more than $2 million in 20 years. Choosing investments over upgrades aligns with the principle of channeling your income into building long-term wealth rather than fleeting satisfaction.

There’s also the psychological trap of the hedonic treadmill. That initial excitement from a bigger house or a luxury car wears off quickly, leaving you back at square one, craving the next upgrade. Instead of chasing that temporary high, stick with your current home and car as long as they meet your needs. Just like automating savings or tracking your spending helps curb financial missteps, resisting lifestyle upgrades safeguards your financial goals and keeps more money working for you in the long run.

5. Make Intentional Purchases

Intentional spending is all about pausing to think before you buy. Ask yourself: Does this purchase help you get closer to your financial goals, or is it just draining your wallet? It's the difference between giving in to impulsive buying and making choices that align with your long-term priorities. When you focus on the value of what you're buying instead of the short-term thrill, you naturally avoid lifestyle inflation.

Take this example: an $800 pair of designer heels. If you invested that $800 at age 25 with a 5% annual return, it could grow to $5,632 by the time you’re 65. That’s the opportunity cost - what you’re giving up by spending the money now instead of letting it grow over time.

To avoid unnecessary purchases, try the one-week rule. For any non-essential item, wait at least seven days before buying. This cooling-off period gives you time to decide if you really need it or if it’s just an impulse.

For bigger purchases, dig deeper into the total cost of ownership. A luxury car might have an appealing sticker price, but don’t forget to account for higher insurance premiums, registration fees, and maintenance costs. Intentional purchasing means looking beyond the initial price tag to understand what you’re committing to financially over time.

Steer clear of impulsive buys, like pricey gym equipment for workouts you haven’t started or designer work clothes for a promotion that hasn’t happened yet. Focus instead on purchases that meet your current needs and align with your financial goals - whether that’s building an emergency fund or saving for early retirement. By keeping this deliberate mindset, you can better protect yourself from lifestyle inflation and stay on track financially.

6. Resist Social Pressure to Spend

Social pressure can be a sneaky culprit behind lifestyle inflation. Whether it’s trying to keep up with friends who prefer pricey restaurants, feeling the need to match a coworker’s designer wardrobe, or getting influenced by social media highlight reels, the pull to overspend is everywhere. The stats back this up: 46% of Gen Z respondents say social spending - like destination weddings or bachelorette parties - plays a major role in blowing their budgets, while nearly 33% of people admit social media ads lead them to overspend. These influences can gradually shift your spending habits without you even realizing it.

The key isn’t to cut yourself off from social connections but to set clear boundaries that align with your financial priorities. One approach gaining traction is “loud budgeting,” a concept that’s been making waves on TikTok. The idea is simple: be upfront about your money goals. For example, when declining an expensive outing, you might say, “I’m focusing on intentional spending.” True friends will respect your honesty, and you might even encourage them to rethink their own spending habits. By aligning your social expenses with your financial goals, you can avoid falling into the trap of lifestyle inflation.

"Your financial priorities should come before social expectations - every time." - Adam Spiegelman, Wealth Advisor

You can also take charge by being the one to suggest plans. Often, the first suggestion sets the tone. Proposing budget-friendly activities like a potluck dinner, a free museum visit, or a hike can make a big difference. Before saying yes to any invitation, take a moment to calculate the full cost - think about travel, outfits, gifts, and meals - so you’re not blindsided later.

Don’t forget to set boundaries online, too. If certain Instagram accounts or influencers tempt you to spend, consider muting or unfollowing them. Disabling one-click purchasing is another great way to curb impulse buys. These small actions can help ensure your social life supports your financial goals instead of derailing them.

sbb-itb-02fd20a

7. Review Your Fixed Expenses Regularly

Fixed expenses are those recurring costs that show up like clockwork - rent, insurance premiums, car payments, cell phone bills, and subscriptions. They’re predictable, which makes it easy to set them on autopilot and forget about them. But here’s the catch: this is exactly where lifestyle inflation sneaks in. As your income grows, you might upgrade to a more expensive apartment, tack on extra streaming services, or sign up for premium memberships. Before you know it, these "structural" costs can quietly take a big bite out of your budget. Even small changes in major expense categories can throw off your financial progress.

It’s not just the big expenses that cause trouble. The real budget killers are the small, recurring subscriptions or services that no longer add value to your life. A $10 monthly subscription might not seem like much, but over a year, that’s $120 - and most people have multiple subscriptions running at the same time. About 50% of U.S. workers say debt payments keep them from saving enough for retirement. These fixed costs aren’t just inconvenient - they’re actively standing in the way of your long-term goals. That’s why it’s critical to review these expenses regularly to plug any hidden leaks in your budget.

"I have seen clients who make more money actually make their financial plans look worse because of lifestyle creep." – Clint Camua, CFP Professional and Regional Director, EP Wealth Advisors

Make it a habit to audit your fixed expenses every three months. Set a calendar reminder and go through your bank and credit card statements to spot unused subscriptions or services. Reach out to your insurance provider, internet company, and cell phone carrier to see if you can secure better rates or take advantage of promotional offers. Just reassessing your insurance needs could save you an average of $83 per month, or nearly $1,000 a year. Once you’ve identified unnecessary or inflated costs, take action. Negotiate with providers - many companies are willing to offer unadvertised discounts of 10% to 20% just to retain your business.

Even small tweaks, like increasing your insurance deductible from $500 to $1,000 or bundling home and auto insurance, can cut costs by up to 25%. Make these reviews a regular part of your routine, especially after major life changes like moving, buying a car, or getting a raise. This way, your fixed expenses stay in check and support your financial goals instead of quietly inflating your lifestyle.

8. Build an Emergency Fund

An emergency fund acts as your financial safety net, shielding you from the pitfalls of lifestyle inflation. Without savings, unexpected expenses - like a car repair, medical bill, or even a sudden job loss - can force you to rely on credit cards or loans. This high-interest debt not only drains your finances but also makes it harder to avoid lifestyle creep once things stabilize. In 2025, data shows that 57% of Americans can't cover a $1,000 emergency without borrowing. Without this buffer, a single crisis could derail your financial progress entirely.

"An emergency fund is what stands between you and high-interest debt when things inevitably go wrong with your home, car, health, or life in general." – Jeremy Zuke, Financial Planner, Abundo Wealth

Experts usually advise saving enough to cover three to six months of essential expenses. These essentials include housing, utilities, groceries, transportation, insurance, and minimum debt payments. According to 2023 data from the U.S. Bureau of Labor Statistics, the average household spends around $6,440 per month, meaning a fully-funded emergency fund should range between $19,320 and $38,640. If you're self-employed or work in an industry with higher risks, consider saving enough for six to twelve months of expenses.

If these numbers feel overwhelming, start small. Aim for an initial goal of $500 to $1,000, which is enough to handle minor emergencies like car repairs or unexpected medical bills. Automate a recurring transfer to your savings account right after payday to make saving easier. For added discipline, keep your emergency fund in a high-yield savings account at a separate bank from your checking account. This reduces the temptation to dip into it for non-urgent expenses.

When you receive a raise or bonus, channel a portion directly into this fund instead of upgrading your lifestyle. By automating contributions, you ensure your financial cushion grows alongside your income, helping you resist lifestyle inflation and stay financially secure.

9. Separate Needs from Wants

Building on mindful spending and intentional purchases, it's important to clearly distinguish between what you need and what you want. This distinction ensures that any extra income goes toward savings instead of unnecessary upgrades.

Needs are the basics required for survival and daily life - things like food, housing, healthcare, and clothing. Wants, on the other hand, are the extras that make life more enjoyable but aren't essential. Think vacations, the latest tech gadgets, or dining out. Social media and advertising often blur the line between these two categories, making it easy to mistake a want for a need.

Failing to separate needs from wants can quickly drain your savings, increase debt, and jeopardize long-term financial security. This is why it's so crucial to understand the difference.

"Knowing how to keep a balance between wants and needs is an important step towards achieving financial stability and freedom." – Edvisors Network

A practical way to maintain this balance is by following the 50/30/20 rule: allocate 50% of your income to needs (like rent and utilities), 30% to wants (like hobbies or entertainment), and 20% to savings. Before making a non-essential purchase, give yourself 48 hours to think it over. Ask questions like, "Am I buying this to impress others?", "Would I still want this if it weren’t payday?", or "Is there a cheaper alternative that meets my needs?"

To make the distinction clearer, consider these examples: a basic cellphone for communication is a need, but the latest high-end smartphone is a want. Similarly, home-cooked meals meet dietary needs, while eating out frequently is a want. A reliable car is necessary for transportation, but opting for a luxury brand veers into the "want" category. By recognizing these differences and budgeting for leisure wisely, you can enjoy life’s perks without letting lifestyle inflation derail your financial goals.

10. Use Accountability Tools

Maintaining discipline in spending often requires the help of accountability systems. These tools - whether it's a budgeting app, a trusted partner, or a financial advisor - can provide the structure and transparency needed to keep lifestyle inflation in check.

Budgeting apps are particularly effective for real-time tracking, helping to curb impulse purchases. By linking your bank and credit card accounts, these tools consolidate your financial data and reveal spending patterns. Many apps use visual aids like color-coded graphs and pie charts to highlight areas where you might be overspending, such as dining out or entertainment. Research shows that 63% of consumers use budgeting tools to gain a clear understanding of where their money goes, and 64% use them to stay accountable to their financial goals.

The impact is clear: users of finance apps report spending 17% less on dining and drinking in their first month of use, with a 14% reduction over the next six months. For example, SmartDollar users save or pay off an average of $16,200 in debt within their first year. Apps like Monefy make it easy to spot problem areas by converting your spending data into clear visuals. Whether it's hidden subscription costs or impulse buys, these insights often lead to a 15-25% reduction in spending simply by increasing awareness.

"External accountability doubles your chances of sticking to limits." – Monefy

But digital tools aren't the only way to build accountability. Sharing your financial goals with someone you trust - a friend, spouse, or financial advisor - can provide the extra motivation needed to stay on track. One Corporate Insight survey respondent shared how these tools help them:

"Their tools are user friendly, keep me organized in a way that makes sense to me and create a reference whenever I am unsure of where I am at with my budget".

To maximize the effectiveness of these tools, consider setting up overspending alerts for discretionary categories, reviewing your app data weekly, and conducting an annual "Lifestyle Audit" to catch unnecessary expenses before they become habits. As David Murphy, Senior Technology Editor at Lifehacker, points out:

"The best advice is not to let the app figure out your financial plan for you".

While these tools provide valuable data, the responsibility to act on it is yours. By staying accountable, you can ensure that your rising income fuels long-term financial stability instead of fleeting indulgences.

Conclusion

Steering clear of lifestyle inflation means directing new income toward building lasting wealth instead of temporary upgrades. The key difference between achieving financial independence and staying stuck on the financial treadmill often lies in how you handle your finances during those critical months after a raise. As Michael Ryan, a retired financial planner, aptly explains:

"Lifestyle creep is what keeps people on the financial treadmill, unable to build wealth despite higher earnings."

Even small spending increases can have a big impact. For instance, a 3% rise in annual expenses could put your retirement at risk. And for every $1,000 added to your yearly spending, you’ll need an extra $25,000 saved to maintain that lifestyle in retirement. On the other hand, modest sacrifices today can grow into major financial freedom down the line.

The strategies outlined here - like automating savings, tracking expenses, and holding yourself accountable - are designed to address lifestyle inflation at its core. Whether you're using tools like Monefy to monitor spending or applying the "First Slice Rule" to allocate raises wisely, the ultimate goal is the same: creating wealth that offers true financial security.

As highlighted throughout this guide, small, deliberate choices can lead to significant financial stability. Keeping your cost of living lower doesn’t just save money - it provides a level of flexibility that no luxury item can replace. It means having the freedom to switch careers, handle unexpected emergencies with confidence, or even retire earlier than most. As MoneyCrashers puts it:

"Real wealth and your ability to change your life lie in your investments, not in an enormous home, fancy car, designer clothes, or the latest gadgets."

FAQs

How much should I automate into savings after a raise?

Automating the process of saving at least 50% of any pay increase is a smart way to build your financial future while keeping lifestyle inflation in check. By directing a portion of your raise straight into a savings or investment account through automatic transfers, you ensure that your financial goals remain a priority. This approach helps you avoid the temptation to spend the additional income and creates a habit of consistent saving.

What spending categories commonly lead to lifestyle creep?

Lifestyle creep often shows up in the form of increased spending on things like dining out, buying luxury brands, upgrading to larger homes, or splurging on more expensive vehicles. As your income rises, it's easy for these discretionary expenses to climb alongside it, which can make saving money and staying on track with financial goals much more challenging.

How do I say no to pricey plans without losing friends?

Saying no to costly plans can feel awkward, but a little honesty paired with respect can make it easier. Be upfront about your financial goals - whether it’s saving for a house or building an emergency fund - and offer budget-friendly alternatives. For example, suggest a cozy get-together at home or a fun outdoor activity instead. Framing your decision as part of a bigger picture helps your friends see where you’re coming from. After all, genuine friends will respect your transparency and cheer you on as you work toward your goals.