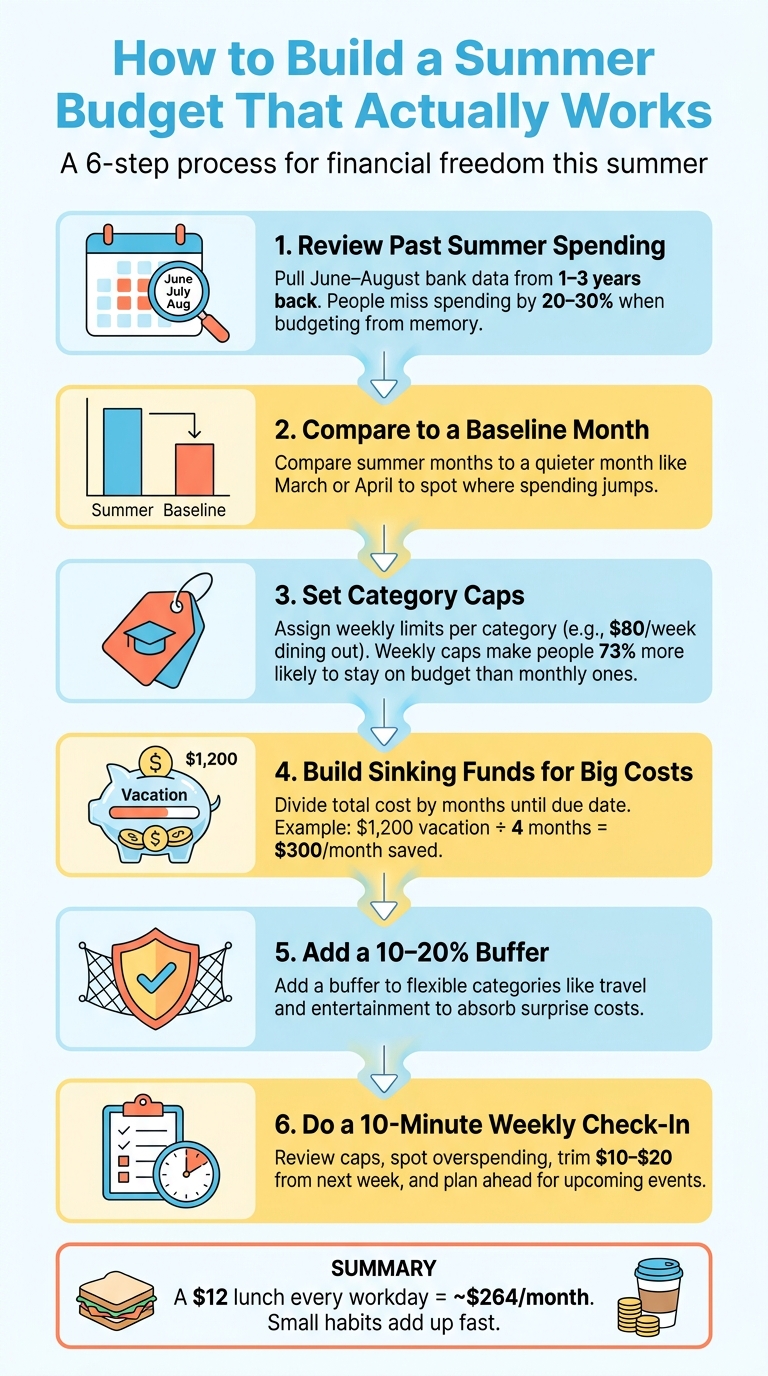

Summer budgets fail for one simple reason: most people plan from memory instead of using their bank data. If I want to stay on track, I need to look at what I spent from June through August, build my limits around those numbers, and check my spending every week.

Here’s the short version:

- I review 1 to 3 years of summer spending.

- I compare summer months with a lower-spend month like March or April.

- I watch the categories that often jump: dining out, travel, gas, utilities, kids’ costs, and entertainment.

- I use weekly caps for day-to-day spending.

- I set up sinking funds for big bills like vacations, camp, and back-to-school shopping.

- I add a 10% to 20% buffer for costs that swing.

- I do a 10-minute check-in once a week.

That matters because people often miss their own spending by 20% to 30% when they budget from memory. And even small habits add up fast: a $12 lunch each workday can hit about $264 a month.

If I keep the plan simple, track spending the same day, and fix small slips early, I have a much better shot at making my budget last all summer.

How to Build a Summer Budget That Actually Works

Review Your Summer Spending Before You Set New Limits

Before you set new limits, start with what you actually spent last summer. Open your bank statements or banking app history for June 1 through August 31 and review the past one to three years. Most banks let you filter transactions by date in the app or online. If you can, download a CSV so you can sort spending by category. Use your statements, not your memory.

Then compare those summer months to a quieter baseline, like March or April. The difference shows where your spending jumps and how much.

Categories That Usually Cost More From June to August

Summer spending usually piles up in a few places. Dining out often climbs with patio season, cookouts, and a busier social calendar. Travel and road trips can jump fast. Kids' activities, including camps and summer child care, often cost more when school is out. Utilities tend to go up because the AC runs longer, and water bills can climb if you're watering a garden. Gas rises with weekend outings and longer drives. And entertainment - concerts, sports games, and outdoor events - can take a bigger bite out of your budget during the summer.

Spotting these categories first is what makes a summer budget work. If you skip them, you're building a plan that doesn't match how summer spending usually plays out.

How to Estimate Your Monthly Summer Total With Real Numbers

Once you know which categories go up, give each one a specific dollar amount based on your statements - not what you hoped to spend. If your dining-out average was $250/month last summer, use $250. If your electric bill was $180 higher in July than in April, add that as a seasonal increase. If you spent $400 on kids' activities in June alone, start there.

It helps to use averages from your last two or three summers so one odd month doesn't throw off the math. After that, add a 15% to 20% buffer to categories that can swing more, like travel and entertainment. That gives you room for the stuff that pops up out of nowhere - a last-minute event invite, a flight delay, souvenirs, or an emergency repair.

Common Summer Expenses: A Comparison Table

Once you've found the categories that rise, turn those numbers into a simple monthly estimate.

| Category | Typical Increase | Best Control Method |

|---|---|---|

| Dining Out | Rises with social events and patio season | Weekly spending cap |

| Travel & Road Trips | Significant spike for vacations and gas | Sinking fund + daily limit |

| Kids' Activities / Camps | High seasonal cost, June–August | Sinking fund (save monthly in advance) |

| Utilities (AC / Water) | Higher electric and water bills from heat | Budget billing or monthly buffer |

| Gas / Transportation | Increases from road trips and outings | Weekly spending cap |

| Entertainment / Concerts | Spikes in outdoor events and treats | Weekly cap within your discretionary budget |

Use these totals as the starting point for the budget you build next.

Build a Summer Budget That Matches Real Life

Turn your summer estimates into category limits. You don’t need to rebuild your budget from scratch. Start with your net take-home pay, then subtract fixed costs like rent or mortgage, insurance premiums, minimum debt payments, and automated savings to figure out how much flexible spending money you have left. That’s your working number.

Add Summer Budget Lines and Shift Money From Lower-Cost Categories

Add summer-specific categories right into your budget, such as Summer Travel, Kids' Activities, Summer Dining Out, and Higher Electric Bill. Then shift money from categories that usually cost less during summer, like heating or indoor entertainment.

Set Spending Caps for Categories That Usually Go Over Budget

Flexible categories like dining out, entertainment, and weekend outings are often where summer spending starts to drift. Set a firm weekly cap, like $80 for dining out or $5 to $15 per day for entertainment. Weekly limits can work better than monthly ones because they’re easier to keep an eye on. In fact, people who use weekly caps instead of monthly ones are 73% more likely to stay on budget.

To find your weekly cap, divide your monthly category limit by 4.33, which is the average number of weeks in a month.

Use Monefy to Track Categories and Budget Limits

Use Monefy to set up your summer categories and log each expense the same day, while the charge is still fresh in your mind. That gives you a better shot at spotting overspending early, before it spills into the rest of your budget. Once those limits are in place, move the bigger seasonal costs into sinking funds.

sbb-itb-02fd20a

Plan Ahead for Big Expenses and Check Your Budget Every Week

Once you've set your category caps, the next move is simple: shift the biggest summer costs into sinking funds.

Use Sinking Funds for Vacations, Camps, and Back-to-School Costs

A sinking fund is money you set aside ahead of time for a specific, predictable expense that doesn't happen every month. The math is simple. Take the total cost, divide it by the number of months or paychecks until the due date, and move that amount on payday so it doesn't get mixed into everyday spending.

For example, if your family vacation will cost $1,200 and you have four months to save, you'd set aside $300 per month. Easy math, less stress. Setting up automatic transfers to a separate savings account with a clear label for that goal can make this even easier.

It's also smart to add a 10% to 15% buffer. That extra cushion can help cover small surprises without forcing you to pull money from other parts of your budget.

Do a 10-Minute Weekly Check-In to Catch Overspending Early

Even if your sinking funds are set up, day-to-day spending can still drift. That's where a short weekly check comes in. A 10-minute review helps you catch overspending sooner than waiting until the end of the month. It also helps protect the category caps and sinking funds you've already put in place.

Here's a simple routine:

- Review (4 mins): Compare your spending with weekly caps in Monefy for categories like dining out and entertainment.

- Spot problem areas (2 mins): Look at the top overspend categories and note any habits or situations that pushed spending off track.

- Adjust (2 mins): Trim $10 to $20 from next week's budget to make up the gap.

- Plan next week (2 mins): Set aside money now for BBQs, trips, or other summer events already on your calendar.

That kind of quick check can stop a small slip from turning into a bigger mess later in the month.

Sinking Fund Table: Monthly Savings Math for Common Summer Costs

| Expense | Total Cost | Date Needed | Monthly Amount to Save |

|---|---|---|---|

| Family Vacation | $1,200 | August 1 | $300 (over 4 months) |

| Summer Day Camp | $600 | June 15 | $200 (over 3 months) |

| Back-to-School Supplies | $300 | August 15 | $75 (over 4 months) |

| Annual Car Registration | $240 | July 1 | $20 (over 12 months) |

Use these numbers as a starting point, then swap in your own costs. The idea is to build big, predictable expenses into the plan before they throw off the rest of your summer budget.

Simple Rules to Spend Less Without Skipping Summer Fun

Limit Paid Outings and Make Free Activities the Default

Once you set your limits, the next step is simple: make day-to-day choices that keep spending from slowly drifting upward. One of the easiest ways to do that is to change your default. Start with free activities, and treat paid outings as the exception, not the plan.

Library programs, community festivals, hiking, and potluck dinners are easy ways to keep summer fun on the calendar without turning every outing into a spending event.

For nonessential purchases, use cash or a dedicated debit card. That creates a hard stop when the money runs out. And if something nonessential costs more than $50, give it 24 hours before you buy it.

That pause matters more than it seems. Entertainment costs can climb fast. A movie ticket or other ticketed event can run $15 to $30 per person, while a park visit or hike may cost little or nothing.

Cut Food and Utility Costs With Small Weekly Habits

Food and utilities are two of the easiest summer categories to rein in.

Food spending, in particular, has a way of sneaking up on people. A $12 lunch each workday adds up to about $264 per month. That’s why simple prep helps. Make five lunches at once and you’re far less likely to grab takeout out of convenience. Five homemade lunches can cost about $30 total, while one restaurant lunch can cost about $15.

If you do eat out, lunch specials are often about half the price of dinner for similar portions. Same meal idea, smaller hit to your budget.

For day trips, pack food before you leave. A cooler with sandwiches and water bottles can save you from convenience-store stops and those last-minute snack runs that always cost more than expected.

At home, utility costs also tend to climb when the weather gets hot. A few small habits can help:

- Close blinds or curtains during the hottest part of the day.

- Run major appliances in the cooler morning or evening hours.

- Add expected summer utility spikes to your budget ahead of time instead of treating them like a surprise.

Conclusion: Track, Adjust, and Keep It Simple All Summer

Staying on budget during the summer usually comes down to a handful of repeatable habits: review what you spent, set category caps that fit real life, use sinking funds for bigger costs like vacations and back-to-school shopping, and check spending often enough to catch problems early.

A quick weekly check-in is usually enough. You don’t need a huge budgeting session. You just need a short moment to see what’s working, what’s off track, and where you need to pull back.

Consistency beats perfection. A budget you follow through most of the summer will work better than a perfect plan that gets dropped by the Fourth of July.

FAQs

How do I budget if last summer was unusual?

If last summer was out of the ordinary, don't base your plan on one month alone. Go through your bank and credit card statements from the past year, look for seasonal spending patterns, then add up your irregular summer costs and divide that total by 12. That gives you a monthly savings target you can work with.

For weekly spending, use your average habits. If your income or costs go up and down, use your lowest usual month instead. Add a 10-15% buffer, and review your budget every Sunday so you can make small adjustments before things drift too far off track.

What should I do if I overspend one week?

If you overspend one week, don’t panic. It’s not a failure. It’s a cue to adjust.

Take a quick look at what caused the extra spending. Was it a true surprise, like an unexpected expense? Or was it an impulse buy you could avoid next time?

From there, make a small course correction. You can:

- Cut back on discretionary spending for the rest of the week, like dining out or entertainment

- Borrow a small, planned amount from next week’s budget

Be sure to record the change. That way, you can spot patterns and fine-tune your spending caps over time.

How many sinking funds do I really need?

You don’t need some magic number of sinking funds. Just set them up for irregular expenses that don’t hit every month but can still throw your budget off if you’re not ready.

That often includes costs like:

- Annual insurance premiums

- Car registrations

- Property taxes

- Car maintenance

- Holiday gifts

Here’s the simple way to do it: list each expense, take the yearly total, divide it by 12, and save that amount every month.

So when the bill shows up, the money is already there. Your main budget stays on track, and you’re not left scrambling to cover it.