If your paycheck runs out before the month does, I’d start with this: track every dollar, cut repeat bills first, trim food and impulse spending, and auto-save even $5 to $25 per payday.

I don’t need more income to start saving. I need a tighter plan for the money I already have. This article shows how to:

- track spending for 30 days

- use a zero-based budget

- set aside money for irregular bills

- lower phone, internet, insurance, and utilities

- spend less on groceries, takeout, and subscriptions

- build a $500 to $1,000 emergency buffer

- put extra cash toward high-interest debt

A few small cuts can add up fast. For example, $25 per month is $300 per year, and $25 per week is $1,300 per year. That kind of buffer matters, especially when 37% of Americans would have trouble covering a $400 emergency without borrowing.

Here’s the big idea in plain English: I don’t have to cut everything. I just need to find the money leaks, stop the easy ones first, and send that cash somewhere better.

Quick snapshot:

| Area | What I’d do first | What it can help with |

|---|---|---|

| Budget | Track all spending for 30 days | Shows where money slips away |

| Fixed bills | Call providers, switch plans, cancel unused charges | Lowers monthly costs |

| Food | Meal plan, buy store brands, cook extra | Cuts grocery and takeout spending |

| Daily habits | Use wait rules and no-spend days | Slows impulse buys |

| Savings | Auto-transfer $5–$25 after payday | Builds an emergency fund |

| Debt | Pay extra on highest APR first | Lowers interest costs |

If I’m on a tight budget, this is the type of plan that gives me a little breathing room without needing a side hustle.

Build a Budget That Shows Where Your Money Goes

Track every dollar for 30 days

Start by looking at where your paycheck already goes. Pull the last 30 to 90 days of bank and credit card statements and review every transaction. Don’t judge any of it. Just write it down. Most households guess their monthly spending wrong by 20–30% before they begin tracking.

Keep it simple. Sort spending into four buckets:

- Housing

- Transportation

- Food

- Everything else

That’s enough to start. You do not need 30 categories on day one. Monefy helps you log and sort purchases as they happen, which makes patterns easier to spot. Frequent takeout, random convenience-store stops, and forgotten auto-renewals tend to show up fast.

Track first, budget second.

After you can see the pattern, plan where each dollar will go before the month starts.

Use zero-based budgeting to assign every dollar a job

With zero-based budgeting, income minus planned expenses equals $0. Every dollar gets a job before the month begins. Cover the basics first: housing, food, utilities, and transportation. Then add debt payments, a small amount for savings, and whatever remains for discretionary spending.

If you’re living paycheck to paycheck, your numbers may look a lot closer to the adjusted version below than the standard 50/30/20 split:

| Budget Category | Standard 50/30/20 | Tight Budget Adjusted |

|---|---|---|

| Needs (Housing, Food, Utilities) | 50% of net income | 60–70% (temporary) |

| Wants (Dining, Entertainment) | 30% of net income | 10–15% |

| Savings & Debt | 20% of net income | 5–10% (to start) |

| Emergency Fund Goal | 3–6 months of expenses | $500–$1,000 (first milestone) |

This kind of budget can feel strict at first. That’s normal. But it gives you a clear view of what your money is doing instead of leaving you to guess at the end of the month.

Add sinking funds and review your budget each month

A sinking fund is money you set aside for bills you know are coming, even if they don’t show up every month. Think car registration, holiday gifts, back-to-school supplies, or an annual insurance premium.

The math is simple. If your car registration costs $180 per year, set aside $15 per month. If holiday gifts usually cost $600, save $50 per month starting in January. Small set-asides now can save you from a nasty hit later.

At the end of the month, open Monefy’s reports and do a quick check-in. Which category went over? Did you skip a sinking fund? A weekly review helps a lot because small overruns are easier to fix before they pile up. Then adjust your limits based on what happened, not what you hoped would happen.

Once your budget is clear, cut the fixed bills and recurring costs that drain it each month.

sbb-itb-02fd20a

Lower Fixed Bills and Recurring Costs

Start with the budget you already built and go after recurring bills first. That’s usually the cleanest place to save, because one cut can keep saving you money every month.

Cut utility and housing-related costs

Home utility costs are a good place to start because small changes can add up fast. Lower your thermostat by one degree in winter - or bump it up by one degree in summer - and you can save about 3% on heating and cooling costs. A programmable thermostat costs about $25 and can pay for itself within a single season.

Lighting is another easy win. LED bulbs use 75% less energy than incandescent bulbs, and a full-home switch can cost under $20. You can also trim costs with simple habits: wash clothes in cold water, run the dishwasher only when it’s completely full, and unplug electronics you’re not using. Standby power costs the average household $100–$200 per year.

If your bills jump during certain times of year, ask your utility provider about budget billing. And if you may qualify, check into LIHEAP.

After home costs, move to the bills you may be able to lower without changing your day-to-day routine.

Negotiate phone, internet, and insurance bills

A lot of monthly bills are more flexible than they look. Internet and cable providers respond to negotiation 70%–80% of the time, and one phone call can save $20–$50 per month. Ask for the retention department, then ask what promotions or discounts are available to lower your bill.

Phone service is another spot where switching plans can pay off. Moving to a low-cost prepaid plan can cut your bill by 40%–60%.

Insurance can also be worth a look. Shopping for new car insurance quotes every 12 months and bundling auto with renters insurance can save 10%–25%. If you already have a small emergency fund, raising your deductible from $500 to $1,000 can lower your monthly premium by $30–$80.

After fixed bills are down, the next place to look is usually groceries, subscriptions, and the small daily purchases that tend to slip by.

Fixed-bill savings options compared

| Bill Type | Typical Monthly Savings | Effort |

|---|---|---|

| Switch to Prepaid Phone Plan | $30–$60 | Low |

| Negotiate Internet/Cable | $20–$50 | Medium |

| Shop/Bundle Car Insurance | $30–$80 | Medium |

| LED Bulbs & Programmable Thermostat | $15–$45 | Low |

| Cancel Unused Subscriptions | $30–$100 | Low |

Once fixed bills are lower, move to groceries, subscriptions, and other everyday spending.

Reduce Everyday Spending Without Feeling Deprived

Small Spending Swaps That Save Big: Monthly & Annual Savings Breakdown

After fixed bills, variable spending is usually the fastest place to cut costs without turning life upside down.

Use meal planning to lower grocery and takeout costs

Food is one of the easiest places to get cash back into your budget. Money slips away fast here. Food waste adds up in the background, and delivery apps can take a $12 meal and turn it into a $19 bill once fees and tips hit.

Start before you even get to the store. Check your pantry, fridge, and freezer first. Then plan 5–7 dinners around what you already have and what’s on sale that week. Low-cost staples like dry beans, rice, lentils, eggs, pasta, potatoes, oats, and frozen vegetables go a long way because they’re cheap, filling, and easy to turn into lots of different meals.

When you cook, make extra. A big pot of chili or soup can cover tonight’s dinner and give you a freezer backup for the night when takeout starts calling your name.

A couple of simple shopping habits help too:

- Shop after eating. Hungry shoppers spend 64% more on impulse foods than people who eat before shopping.

- Check the unit price, not just the shelf price. Cost per ounce or pound tells you what’s cheaper.

- Reach for store brands when it makes sense. They’re usually 15–30% cheaper than name brands and are often made by the same manufacturers.

Once food spending starts to settle down, the next place to look is recurring charges and impulse spending.

Audit subscriptions and set spending rules

Recurring variable spending has a way of hiding in plain sight. Streaming services, apps, and memberships can just keep rolling month after month.

Pull up the last two months of bank statements and mark every recurring charge. If you haven’t used something in the last 30 days, cancel it. If you miss it later, you can always sign up again.

For streaming, don’t stack everything at once. Rotate. Subscribe to one service, watch what you want, cancel it, then switch to another the next month. It’s a simple move, but it keeps monthly costs from creeping up.

Impulse spending needs a speed bump too. Use a 24-hour rule for small purchases and a 48-hour rule for anything over $25. That short pause can cut out 50–70% of impulse buys. And if you track recurring charges in Monefy, they’re much harder to ignore when they show up again.

Small spending swaps that free up cash

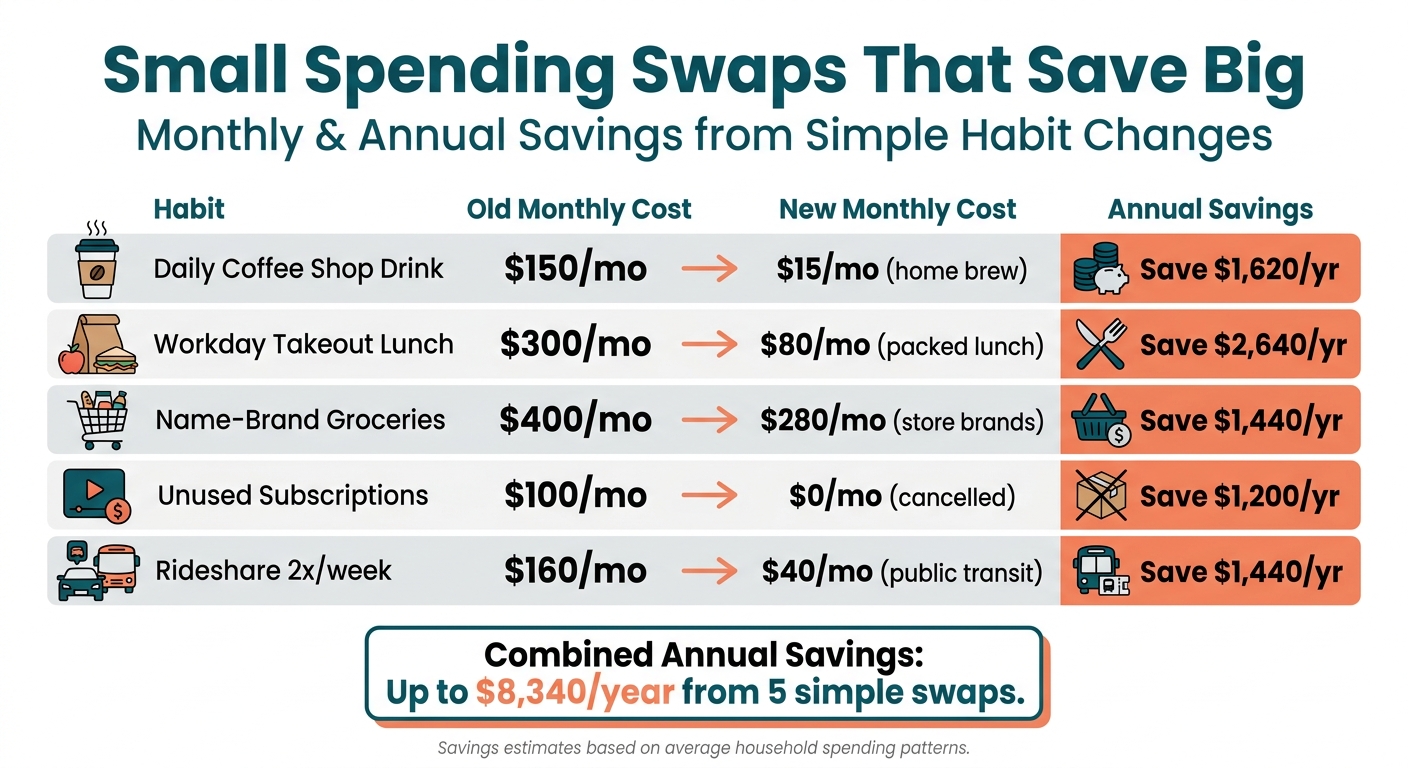

Small daily habits often do more for your budget than one big dramatic cut. A coffee shop run feels harmless until you do the math. Brewing coffee at home costs about $0.25–$0.50 per cup, compared with $5.00 at a coffee shop. Lunch works the same way: packing it costs about $3.00–$5.00 per meal, while takeout runs $12.00–$15.00.

| Habit | Old Monthly Cost | New Monthly Cost | Monthly Savings | Annual Savings |

|---|---|---|---|---|

| Daily Coffee Shop Drink | $150 | $15 (home brew) | $135 | $1,620 |

| Workday Takeout Lunch | $300 | $80 (packed) | $220 | $2,640 |

| Name-Brand Groceries | $400 | $280 (store brands) | $120 | $1,440 |

| Unused Subscriptions | $100 | $0 (cancelled) | $100 | $1,200 |

| Rideshare (2x/week) | $160 | $40 (public transit) | $120 | $1,440 |

One more rule that helps: set one no-spend day each week. No takeout, no shopping, no rideshares. It breaks the habit of spending by default and pushes you to use what you already have at home.

Automate Savings, Pay Down Debt, and Start a Simple Action Plan

Start with small automatic transfers and build an emergency fund

After you cut costs, put that extra money on autopilot. Set up a transfer of $5 to $25 into a separate savings account for the day after payday. The amount matters less than the habit. A $25 weekly transfer turns into $1,300 over one year without much effort.

Want to make that money less tempting to touch? Keep the savings account at a different bank than your checking account. That extra step can help you leave it alone.

Build your buffer in this order:

| Buffer Level | Target | Purpose |

|---|---|---|

| Level 1 | $500 | Small emergencies |

| Level 2 | $1,000 | Short-term buffer |

| Level 3 | 1 month of expenses | Income disruption |

It also helps to name the account something specific, like "Car Repair Fund" or "$500 Buffer." That small detail makes the goal feel concrete instead of abstract.

Put freed-up cash toward high-interest debt first

Once you have a starter buffer, send extra cash to debt. Keep paying the minimum on every balance, then direct all extra money to the card with the highest interest rate first. That's the Debt Avalanche method: pay the highest-interest debt first.

If you've been carrying a balance for a while, it's worth making one phone call. Ask your card issuer's hardship department for a lower APR. 76% of cardholders who asked got one, and the average cut was 6.3 percentage points.

Then turn the plan into a simple weekly rhythm.

Follow a 7-day starter plan and recap the key steps

Use the next seven days to get the system running:

- Day 1-2: Keep logging every transaction in Monefy.

- Day 3: Pull recent bank statements, spot forgotten subscriptions and fees, and cancel what you no longer use.

- Day 4: Call your internet, phone, or insurance provider and ask for a lower rate or retention discount.

- Day 5: Apply your zero-based budget to this month's income.

- Day 6: Set up a $5 to $25 automatic transfer into a separate savings account for the day after payday.

- Day 7: List your debts from highest to lowest interest rate and mark the first balance to attack.

- Ongoing: Set a weekly review reminder so you can catch overspending early.

FAQs

What if I can only save $5 a week?

Saving $5 a week is still a solid start. Building a financial safety net comes down to consistency, not how big the amount is at the start.

Set up an automatic transfer to a separate savings account as soon as your income hits. That way, saving happens in the background and takes less effort. When your budget gives you a little more room, bump it up by $5 or $10 over time.

How do I budget for bills that don’t happen every month?

Use a sinking fund for bills that don’t show up every month. Write down the non-monthly costs you expect during the year, like annual subscriptions or car maintenance. Then add them up and divide the total by 12.

Set that amount aside each month so the money is there when the bill hits. It’s a simple way to stop surprise costs from messing up your budget.

Should I save first or pay off debt first?

If you're living paycheck to paycheck, begin with a $500 emergency fund before you go hard on debt payoff. It may seem small, but that cash cushion can help you cover surprise costs without swiping a credit card.

Once that buffer is in place, turn your attention to high-interest debt first. While you do that, keep making every required minimum payment so you don't fall behind or end up in collections.