If you want to reduce your tax bill while supporting charities, donor-advised funds (DAFs) can be a game-changer. Here's what you need to know:

- Immediate Tax Benefits: Get a deduction in the year you contribute, even if you distribute funds to charities later.

- Avoid Capital Gains Taxes: Donate appreciated assets like stocks and deduct their full market value.

- Flexible Giving: Contribute during high-income years or use a "bunching" strategy to exceed the standard deduction.

DAFs are perfect for high earners, investors with appreciated assets, or anyone experiencing income spikes. Whether you're donating stocks, cash, or other assets, timing and strategy are key to maximizing savings.

Learn how to set up a DAF, choose the right assets, and plan contributions to get the most out of this powerful tool for philanthropy and tax savings.

Timing Contributions to Get the Most Tax Savings

When you contribute to a Donor-Advised Fund (DAF), timing is just as critical as the amount you give. The right timing can transform a regular tax deduction into a much larger savings opportunity. By leveraging strategies like contributing during high-income years and using the bunching method, you can maximize the tax benefits tied to your donations.

Contributing During High-Income Years

The most effective time to fund a DAF is during a year when your income is unusually high. Events like selling a business, receiving a large bonus, vesting restricted stock units (RSUs), or completing a Roth conversion often push you into a higher tax bracket. In these years, the value of a charitable deduction increases significantly because it offsets income taxed at the highest marginal rates.

Take Marcus, a senior tech executive, as an example. In 2026, he donated 2,000 shares of employer stock valued at $280,000 (with a $28,000 cost basis) to a DAF during a high-income year when his RSUs vested. By timing his donation strategically, Marcus avoided $59,640 in capital gains tax, saved $103,600 in income tax (at a 37% rate), and eliminated $9,576 in Net Investment Income Tax (NIIT). His total tax savings? $172,816.

To ensure your contributions count for the tax year, initiate appreciated stock transfers by December 20. These transfers typically require 3–5 business days to settle, and the process must be completed by December 31.

Beyond high-income years, the bunching strategy offers another way to optimize your tax savings.

Using the Bunching Strategy

The bunching strategy involves consolidating several years' worth of charitable contributions into a single tax year. Instead of giving $10,000 annually, you might contribute three to five years' worth of donations to your DAF in one year. Afterward, you can use the DAF to distribute grants to your preferred charities incrementally, ensuring they receive steady support while you claim a larger deduction upfront.

"A donor-advised fund (DAF) allows you to 'bunch' multiple years of charitable contributions into a single tax year, pushing your itemized deductions above the standard deduction threshold." - Michael Ruger, Partner, Greenbush Financial Group

For the roughly 90% of taxpayers who take the standard deduction, annual charitable donations often provide no additional tax benefits. Let’s break it down: A married couple donating $10,000 annually would claim the standard deduction each year, totaling $96,600 over three years. But by bunching $30,000 into Year 1 (alongside $15,000 in other itemized deductions like SALT and mortgage interest), they could claim $45,000 in itemized deductions that year and revert to the standard deduction for Years 2 and 3. Their three-year total deduction would jump to $109,400.

| Scenario | Year 1 Deduction | Year 2 Deduction | Year 3 Deduction | 3-Year Total |

|---|---|---|---|---|

| Annual $10,000 gift | $32,200 (Standard) | $32,200 (Standard) | $32,200 (Standard) | $96,600 |

| Bunched $30,000 gift | $45,000 (Itemized)* | $32,200 (Standard) | $32,200 (Standard) | $109,400 |

*Assumes $15,000 in other itemized deductions (SALT/mortgage interest).

One key update to note for 2026: under the One Big Beautiful Bill Act (OBBBA), a new 0.5% AGI floor applies to itemized charitable deductions. This means only the portion of your donations exceeding 0.5% of your Adjusted Gross Income (AGI) is eligible for a deduction. For most donors using the bunching strategy, this threshold is easy to surpass, but it’s an important detail to include in your planning.

"Giving to a donor-advised fund has the added benefit of allowing individuals to avoid capital gain by gifting appreciated assets. This provides a dual income tax benefit when combined with bunching." - Molly Petitjean, Charitable Solutions consultant, Thrivent Charitable

sbb-itb-02fd20a

Choosing the Right Assets to Donate

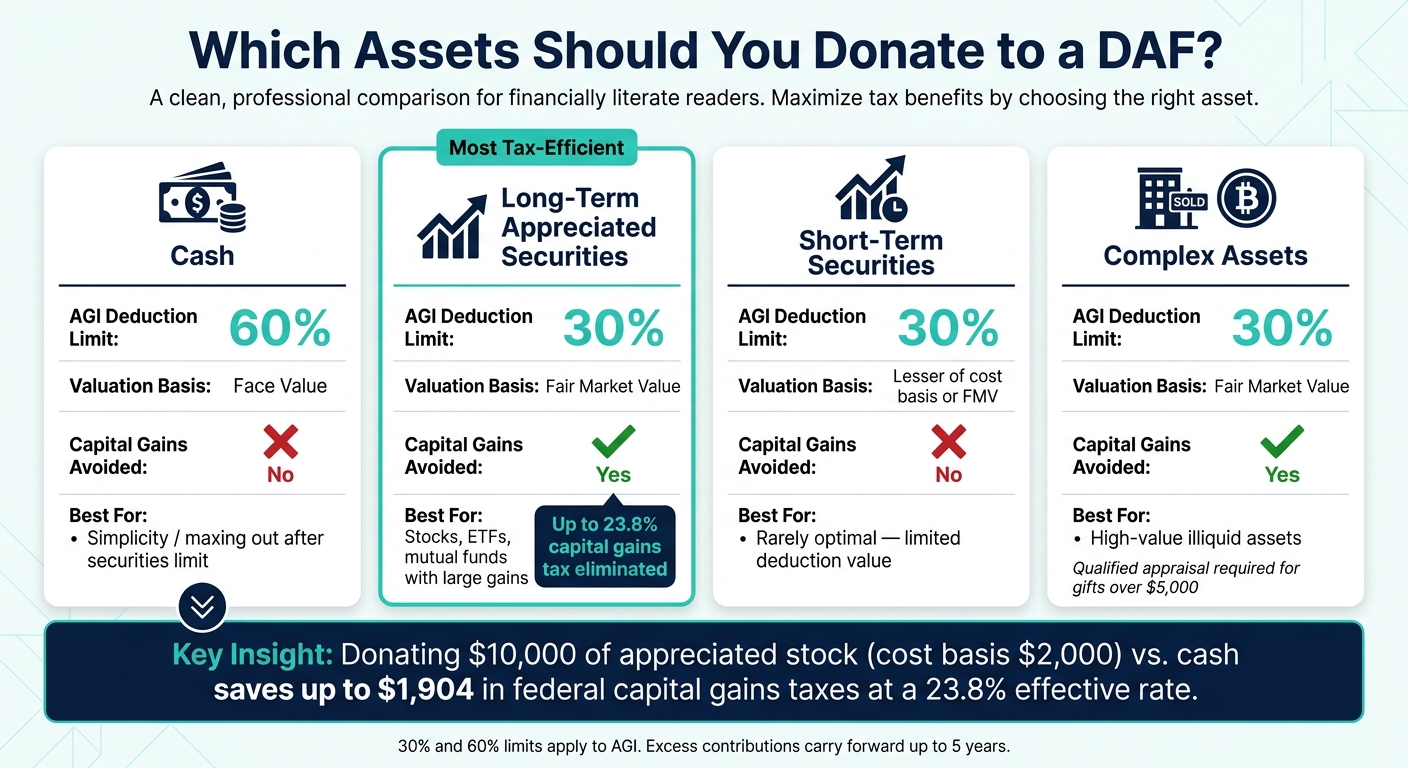

DAF Asset Types: Tax Deduction Limits & Capital Gains Benefits

Selecting the right assets to donate is just as important as timing when it comes to maximizing the tax benefits of your donor-advised fund (DAF). Different types of assets offer varying advantages, so understanding these options can help you make the most of your charitable contributions.

Donating Appreciated Securities

Long-term appreciated securities - such as stocks, ETFs, and mutual funds held for more than a year - are among the most tax-efficient assets to donate. By transferring these directly to a DAF, you avoid federal capital gains taxes (up to 20%), the 3.8% Net Investment Income Tax (NIIT), and any applicable state taxes. Plus, you can deduct the full fair market value (FMV) of the shares instead of just your original cost basis.

Here’s an example to illustrate: If you donate $10,000 worth of stock with a $2,000 cost basis, you get the same $10,000 deduction as you would with a cash gift. However, you also eliminate up to $1,904 in federal capital gains taxes, assuming a 23.8% effective tax rate. This strategy can also simplify portfolio rebalancing by allowing you to donate highly appreciated shares without triggering capital gains taxes. As Brandon O'Neill from Fidelity Charitable puts it:

"Instead of simply selling long-term appreciated securities, periodically cherry-pick the ones with the most appreciation and donate them to a public charity with a donor-advised fund program instead."

It’s essential to hold securities for at least one year and one day before donating. If you donate securities held for less than a year, your deduction is limited to the lesser of your cost basis or FMV, which significantly reduces the benefit.

Cash Contributions and AGI Limits

Cash donations are the simplest to make but don’t offer the added benefit of avoiding capital gains taxes. However, cash gifts come with a higher adjusted gross income (AGI) deduction limit - up to 60%, compared to 30% for appreciated securities. This is particularly helpful if you’ve already maxed out the 30% limit for non-cash assets or don’t have appreciated holdings to donate.

Starting in 2026, non-itemizers can also claim a deduction for cash gifts up to $1,000 ($2,000 for joint filers) above the line, though this option doesn’t apply to DAF contributions.

| Asset Type | AGI Deduction Limit | Valuation Basis | Capital Gains Avoided? |

|---|---|---|---|

| Cash | 60% | Face value | No |

| Appreciated Securities (>1 yr) | 30% | Fair Market Value | Yes |

| Short-Term Securities (<1 yr) | 30% | Lesser of cost basis or FMV | No |

| Complex Assets (Real Estate, Private Biz) | 30% | Fair Market Value* | Yes |

*A qualified appraisal is required for gifts over $5,000.

Other Non-Cash Assets

DAFs can accept a surprising variety of non-cash assets, including real estate, private business interests (such as C-corp or S-corp shares), partnership interests (LP/LLC), and cryptocurrency. Like appreciated securities, these assets are deductible at FMV and help you avoid capital gains taxes, though they are subject to the same 30% AGI limit.

For non-cash contributions valued over $5,000, a qualified appraisal is necessary to claim the deduction. Donating S-corporation stock can be tricky, as it may result in Unrelated Business Taxable Income (UBTI), so consulting with a tax advisor is highly recommended. Additionally, cryptocurrency donations over $5,000 require a formal appraisal, not just the exchange price.

If you hold assets that have lost value, it’s better to sell them first to harvest the tax loss. This loss can offset other capital gains or reduce up to $3,000 of ordinary income annually. You can then donate the cash proceeds to your DAF, maximizing your tax benefits.

How to Set Up and Manage a DAF Contribution

Setting Up a DAF Account

Starting a donor-advised fund (DAF) is straightforward. The first step is selecting a sponsoring organization, which is a qualified 501(c)(3) entity that manages the fund for you. Your options include national providers like Fidelity Charitable, Schwab Charitable, or Vanguard Charitable, as well as local community foundations or faith-based groups.

Before choosing, compare the minimums and fees of various sponsors:

| Sponsoring Organization | Minimum to Open | Annual Admin Fee (first $500K) | Minimum Grant |

|---|---|---|---|

| Fidelity Charitable | $0 | 0.60% (min $100/year) | $50 |

| Schwab Charitable | $0 | 0.60% | $50 |

| Vanguard Charitable | $25,000 | 0.60% | $500 |

| Daffy | $0 | $36–$240 flat rate | $18 |

Most applications can be completed online in as little as 5–15 minutes. You'll need to provide your legal name, contact details, and a name for the account (e.g., "The Johnson Family Giving Fund"). Additionally, you'll designate successor advisors or charities to manage the fund after your death and choose an initial investment strategy.

Once you contribute assets to the DAF, they legally belong to the sponsoring charity. This irrevocable transfer is what makes your contribution eligible for a tax deduction at the time of donation. This simple process not only secures your tax benefits but also sets the stage for long-term charitable giving.

Funding the DAF

After opening your account, the next step is transferring assets, which can significantly impact your tax situation.

For appreciated securities, transfer the shares directly to your DAF to avoid triggering capital gains taxes. As Kenneth Dennis emphasizes:

"The most critical rule: do not sell the shares before transferring. Selling triggers capital gains tax immediately, destroying the core benefit of this strategy."

Cash contributions can be made via check, wire transfer, or EFT. While this method is straightforward, it doesn't provide the tax advantage of avoiding capital gains taxes like appreciated securities.

Timing is another key consideration. For standard stock transfers, initiate the process by December 20 to ensure completion before the December 31 tax deadline. For more complex assets, such as real estate or private business interests, it's best to start by November 30.

Your sponsoring organization will provide a written acknowledgment of your contribution, which you’ll need for tax purposes. For non-cash contributions over $500, you'll also need to file Form 8283. Additionally, assets valued at more than $5,000 (excluding publicly traded stocks) typically require a qualified appraisal.

Once funded, your DAF allows you to schedule grants at your convenience.

Making Grants Over Time

A major advantage of a DAF is that you can claim an immediate tax deduction while deciding on grants later. This flexibility lets you recommend grants to charities on your own schedule, whether that’s next month or several years from now.

To recommend a grant, log into your DAF's online portal, search for an eligible 501(c)(3) charity, and specify the donation amount and purpose. The sponsoring organization will verify the charity's status and usually distribute the funds within 10 business days. As Phil DeMuth, author of The Tax Smart Donor, explains:

"Donating from a DAF is basically as simple as online bill pay."

While waiting to distribute funds, you can invest your DAF assets in options like stocks, bonds, or ESG funds. Any growth on these investments is tax-free. For example, if a $50,000 contribution grows to $65,000, the entire $65,000 can eventually be donated to charity. However, DAF funds cannot be used for personal benefits, such as gala tickets or tuition, or to fulfill binding personal pledges.

You can also name successor advisors, such as a spouse or children, to continue grant-making after you’re gone. This feature allows a DAF to serve as a multi-generational giving tool, offering a simpler alternative to managing a private foundation.

Tax Reporting and Compliance for DAFs

Once you've funded your Donor-Advised Fund (DAF) and scheduled your grants, the next step is to ensure your contributions are accurately reported for tax purposes. Proper reporting not only secures your immediate tax benefits but also helps maintain savings over time.

Itemizing Deductions for Maximum Savings

To claim a deduction for your DAF contributions, you'll need to itemize deductions using Schedule A of Form 1040. However, the total of your itemized deductions must exceed the standard deduction for the 2026 tax year before your DAF contributions can provide any tax advantage.

For 2026, the standard deduction is set at $15,750 for single filers and $31,500 for married couples filing jointly. Additionally, only charitable contributions exceeding 0.5% of your Adjusted Gross Income (AGI) are deductible. Tim Johnson, CPA and Partner at JLK Rosenberger, explains:

"Starting in 2026, taxpayers will have a floor to get over before a charitable contribution is deductible. Only the portion of charitable contributions that exceed 0.5% of Adjusted Gross Income (AGI) is net deductible starting in 2026."

For instance, if your AGI is $200,000, the first $1,000 of charitable donations won't be deductible. Furthermore, for taxpayers in the top 37% bracket, the federal tax benefit of charitable deductions will be capped at 35% in 2026.

Make sure to report cash contributions on Schedule A, Line 11, and non-cash contributions on Line 12.

Staying Within IRS Contribution Limits

The IRS places annual limits on how much of your DAF contributions can be deducted based on your AGI. Here's a quick breakdown for 2026:

| Asset Type | Deduction Limit | Valuation Method |

|---|---|---|

| Cash | 60% of AGI | Face value |

| Long-term appreciated stock (>1 year) | 30% of AGI | Fair market value |

| Short-term stock (≤1 year) | 30% of AGI | Cost basis only |

| Complex assets (real estate, crypto) | 30% of AGI | Fair market value (requires appraisal) |

If your contributions exceed these limits, the excess can be carried forward for up to five additional tax years.

For contributions of $250 or more, obtain a Contemporaneous Written Acknowledgment (CWA) from your DAF sponsor. Without this documentation, the IRS can disallow the deduction. Megan Robinson, FPQP™ at SDT Planning, emphasizes:

"The IRS can disallow deductions of $250+ without a contemporaneous written acknowledgment."

The CWA must confirm the amount and date of the contribution, state that the sponsoring organization has exclusive control over the assets, and disclose whether any goods or services were received in return. For non-cash contributions over $500, you'll need to file Form 8283, and if the value exceeds $5,000 (except for publicly traded securities), a qualified appraisal must also be included.

Tracking Contributions with Tools Like Monefy

Keeping organized records of your DAF contributions, carryforwards, and supporting documents is essential for meeting IRS requirements and maximizing your deductions. Apps like Monefy can help you:

- Categorize contributions

- Store CWA letters digitally

- Track carryforward balances

This kind of ongoing tracking is especially useful if you're using strategies like bunching or managing complex assets. By monitoring your AGI limits and carryforward amounts, you can better plan whether to accelerate contributions in a given year or rely on carryforwards in the future. Staying on top of these details ensures you're well-positioned to maximize your tax savings through thoughtful, disciplined planning.

Conclusion and Final Tips

Key Takeaways for Donor-Advised Funds

Donor-advised funds (DAFs) shine when used as both a tax-saving tool and a long-term vehicle for giving. To maximize their potential, focus on three key strategies: bundling multiple years of donations into one to surpass the standard deduction, contributing appreciated securities instead of cash to sidestep capital gains taxes, and timing large contributions during high-income years for the greatest tax benefit.

As Clete Albitz, CFA, CFP®, from Albitz & Miloe, explains:

"The power of a DAF lies in its ability to separate the timing of the tax deduction from the timing of the charitable impact."

This flexibility allows you to claim deductions when they're most advantageous while controlling when and how grants are distributed. Additionally, repurchasing shares with cash after donating appreciated securities resets your cost basis, helping to minimize future capital gains. These immediate benefits create a solid foundation for a thoughtful, long-term giving plan.

Planning Long-Term Charitable Giving

DAFs aren't just for short-term tax planning; they can serve as the cornerstone of your philanthropic efforts for years to come. Brandon O'Neill, Vice President at Fidelity Charitable, emphasizes this point:

"The year they sell their business is typically the biggest tax year of their life. They can fund charitable giving potentially for the rest of their life by setting aside some of that business stock prior to it being sold."

With DAFs currently holding around $326 billion in assets, many donors are shifting toward viewing these accounts as tools for sustained giving rather than one-time contributions. Setting up recurring contributions - even small ones - can steadily grow your charitable fund without requiring frequent decisions.

Lastly, don't forget about succession planning. By naming a successor advisor or a charity as the beneficiary of your DAF, you ensure your philanthropic vision continues beyond your lifetime. This simple step can turn a tax-focused strategy into a legacy of generosity.

FAQs

Can I deduct a DAF gift now but give to charities later?

Yes, you can take a tax deduction in the same year you contribute to a donor-advised fund, even if you decide to distribute the funds to charities at a later time. This approach lets you claim the deduction during a high-income year while giving you the freedom to donate to nonprofits at your own pace. Using tools like Monefy can make it easier to track these contributions and ensure they align with your broader financial plans.

What’s the best way to donate stocks to avoid capital gains tax?

If you want to sidestep capital gains tax, consider transferring long-term appreciated stocks directly to a donor-advised fund (DAF) rather than selling them. This approach allows you to claim a tax deduction for the stock's full fair market value while bypassing capital gains tax and the 3.8% Net Investment Income Tax. Just make sure the transfer is completed before any sale agreement is finalized. Tools like Monefy can assist in tracking your assets and planning your contributions with ease.

How does bunching donations help me beat the standard deduction?

Bunching donations is a strategy that allows you to consolidate multiple years' worth of charitable contributions into a single tax year. By doing this, you can push your itemized deductions - like mortgage interest and state taxes - beyond the standard deduction limit, which can lead to increased tax savings. In the years that follow, you can then revert to taking the standard deduction. Using a donor-advised fund can make this approach even more effective, as it enables you to continue supporting your favorite charities annually while still reaping the tax advantages in the year you choose to bunch your donations.