Your credit score directly impacts the mortgage rate you qualify for. A higher score means lower interest rates, saving you tens of thousands over the life of a loan. For example:

- A 760–850 FICO® Score could secure a 6.70% APR on a 30-year mortgage.

- A lower score of 620–639 might lead to a 7.36% APR, costing an extra $60,000 in interest on a $378,384 loan.

Banks and lenders use your median credit score from the three major bureaus (Equifax, Experian, TransUnion) to determine your rate. Even minor improvements, like moving from 719 to 720, can lower rates and save thousands. To improve your score:

- Pay down credit card balances (keep utilization below 10%).

- Fix errors on your credit report early.

- Avoid new credit inquiries before applying.

Lenders also adjust fees based on credit tiers. Borrowers with scores above 760 may receive discounts, while those below 640 face higher costs and stricter terms. Good credit preparation is essential to securing favorable rates and minimizing long-term costs.

How Lenders Use Credit Scores to Set Mortgage Rates

When you apply for a mortgage, lenders don’t just look at a single credit score. Instead, they pull a "tri-merge" credit report, which combines data from Equifax, Experian, and TransUnion. From this, they use your middle (median) score to determine your rate and eligibility. If only two scores are available, they’ll use the lower one. For joint applications, each borrower’s median score is calculated, and the lower of the two is used to price the loan. This approach directly impacts your mortgage rate.

"Mortgage lenders pull reports from all three major credit bureaus and use your middle score. If you're buying with someone else, they take both middle scores and use the lower one." - ConsumerAffairs

Even a small error on one bureau’s report can lower your median score, potentially leading to a higher interest rate.

Credit Scoring Models Used in Mortgage Underwriting

Most lenders currently rely on Classic FICO models: FICO Score 2 (Experian), FICO Score 5 (Equifax), and FICO Score 4 (TransUnion). These models are widely trusted, with about 90% of top lenders using FICO scores for mortgage decisions. However, change is on the horizon. The Federal Housing Finance Agency (FHFA) has announced that lenders will transition to newer models - FICO 10T and VantageScore 4.0 - for loans sold to Fannie Mae and Freddie Mac.

These updated models differ from the Classic versions by incorporating trended data, which looks at your payment behavior over time rather than just providing a snapshot. This shift, expected to roll out by early 2025, could open up opportunities for around 5 million buyers with limited or thin credit histories.

Credit Score Tiers and Their Effect on Interest Rates

Mortgage rates don’t adjust on a smooth, continuous scale. Instead, they follow 20-point increments. For example, moving from a score of 719 to 720 might land you in a better pricing tier with a lower interest rate.

"The credit score scale is sliced up into 20-point increments. A borrower's rate adjusts with each 20-point move up or down the scale." - Rob Kaufman, myFICO

Here’s how these tiers impact a 30-year conventional mortgage for a $350,000 loan (as of May 2026):

| FICO® Score | 30-Year Conventional APR | Monthly Payment (on $350,000) |

|---|---|---|

| 760–850 | 6.51% | $1,772 |

| 700–759 | 6.76% | $1,818 |

| 680–699 | 6.87% | $1,838 |

| 660–679 | 6.94% | $1,852 |

| 640–659 | 7.06% | $1,874 |

| 620–639 | 7.21% | $1,903 |

Source: Curinos data via Experian

Lenders also factor in Loan-Level Price Adjustments (LLPAs), which are fees tied to risk factors like your credit score. For example, borrowers with a score of 780 or higher might see a –0.25% fee adjustment, while those in the 620–639 range could face a +3.25% adjustment. On a $350,000 loan, this could mean over $11,000 in extra costs before even considering interest.

The bottom line: if your median score is close to the next tier - say 718 - it’s worth working to bump it up to 720. That small improvement could translate into meaningful savings on your monthly payment and thousands over the life of your mortgage. Using a personal finance app can help you track expenses and reach these savings goals faster.

sbb-itb-02fd20a

The Long-Term Cost of a Low Credit Score on a Mortgage

How Your Credit Score Affects Mortgage Rates & Total Cost

Over a 30-year mortgage, even a slight difference in interest rates can lead to tens of thousands of dollars in extra costs.

How Different Credit Score Ranges Affect Mortgage Costs

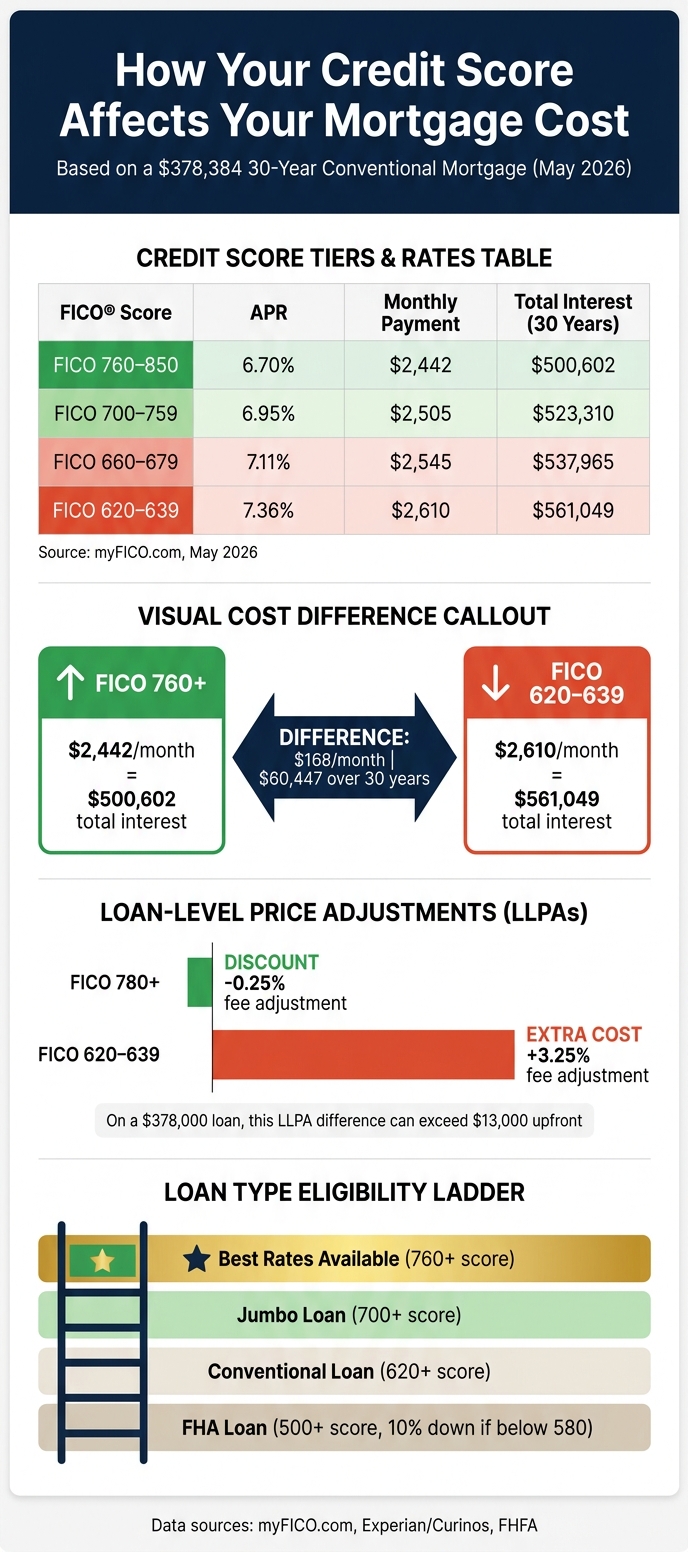

Let’s compare two borrowers taking out the same $378,384 loan in May 2026. One has a FICO® score of 760, while the other scores 620. The borrower with the higher score secures a 6.70% APR, resulting in a monthly payment of $2,442. Meanwhile, the lower-score borrower gets a 7.36% APR and pays $2,610 per month. That’s an extra $168 each month - or $60,447 in additional interest over the life of the loan. This highlights how a lower credit score increases both monthly payments and long-term costs.

| FICO® Score | APR | Monthly Payment | Total Interest (30 Years) |

|---|---|---|---|

| 760–850 | 6.70% | $2,442 | $500,602 |

| 700–759 | 6.95% | $2,505 | $523,310 |

| 660–679 | 7.11% | $2,545 | $537,965 |

| 620–639 | 7.36% | $2,610 | $561,049 |

Source: myFICO.com data, May 2026

"The total interest paid differs by $60,980! That's a lot of extra interest to pay because of a low credit score." - Rob Kaufman, Writer, myFICO

In states with higher housing costs, like California or Hawaii, the financial gap can surpass $40,000. These added costs often push lenders to impose stricter terms on borrowers with lower credit scores.

How Low Credit Scores Lead to Stricter Loan Terms

A low credit score doesn’t just mean higher interest rates - it also brings additional fees and tighter borrowing conditions. Lenders view lower scores as riskier, prompting them to adjust loan terms accordingly.

For conventional loans, Loan-Level Price Adjustments (LLPAs) are fees that increase with credit risk. A borrower with a score between 620 and 639 might face a 3.25% LLPA fee and Private Mortgage Insurance (PMI) costs of $140 to $200 per $100,000 borrowed. In contrast, borrowers with scores above 760 may receive a –0.25% LLPA credit and PMI costs as low as $30 to $45 per $100,000. On a $378,000 loan, this LLPA difference alone can exceed $13,000 upfront.

Credit scores also determine eligibility for different types of loans:

- Conventional loans require a minimum score of 620.

- Jumbo loans usually demand scores of 700 or higher.

- FHA loans allow scores as low as 500, but borrowers with scores below 580 must make a 10% down payment.

"This data reinforces just how central credit preparation is to homebuying affordability. Two borrowers with similar incomes can experience dramatically different buying power depending on their credit score." - Max Slyusarchuk, CEO, AD Mortgage

Common Credit Problems That Drive Up Mortgage Rates

Credit score issues often stem from recurring habits, and they can take time to build up. Knowing which factors hurt your score the most can help you focus your efforts on improving it.

High Credit Utilization

Credit utilization - how much of your available credit you're using - makes up 30% of your FICO® Score. It's second only to payment history in importance. Lenders see high balances as a potential sign of financial strain, which can lower your score and lead to higher mortgage rates. To improve your score, aim to keep your credit utilization below 10%. Mortgage Loan Officer Dean Rathbun from United American Mortgage Corporation emphasizes:

"Making your payments on time is the most important factor of credit. The second is keeping your (credit card) balances down to 30% or less of the high limit of the credit item."

One way to lower your reported balances quickly is to pay down your credit card balances before the statement closing date, as that's when creditors report to the bureaus. Also, avoid closing old credit cards before applying for a mortgage. Closing accounts reduces your total available credit, increases your utilization ratio, and shortens your credit history - all of which can hurt your score. These factors, combined with missed payments, can make it harder to qualify for favorable mortgage rates.

Missed Payments and Delinquencies

Payment history carries the most weight in your FICO® Score, accounting for 35% of it. Payments must be at least 30 days late before they show up on your credit report and start affecting your score. Once reported, a late payment can remain on your report for up to seven years, with recent missed payments having the most significant impact on your mortgage rate. Setting up autopay for at least the minimum payment on all your accounts can help you maintain a steady on-time payment record before applying for a mortgage. Additionally, reviewing your credit report for accuracy is crucial to avoid unnecessary rate increases.

Errors on Your Credit Report

Errors on your credit report can also hurt your chances of securing a good mortgage rate. A Federal Trade Commission study found that about 26% of participants spotted at least one error on their credit report that could make them seem riskier to lenders. These errors could range from payments wrongly marked as late to accounts that don’t belong to you, potentially costing you thousands in extra interest.

To catch these mistakes early, request your credit reports from all three bureaus - Equifax, Experian, and TransUnion - through AnnualCreditReport.com. Ideally, do this 6 to 12 months before applying for a mortgage. If you find errors, dispute them with both the credit bureau and the original creditor. Under the Fair Credit Reporting Act (FCRA), credit bureaus generally have 30 days to investigate disputes, which can extend to 45 days if you provide additional details. Be aware that having "account in dispute" notations on your report can cause issues with mortgage underwriters, so resolve disputes well before you apply. If you discover errors close to your closing date, ask your lender about a rapid rescore. This process can update your credit report within 2 to 5 business days, though it costs $25 to $50 per account, per bureau.

| Credit Bureau | Dispute Mailing Address | Phone Number |

|---|---|---|

| Equifax | P.O. Box 740256, Atlanta, GA 30348 | 866-349-5191 |

| Experian | P.O. Box 4500, Allen, TX 75013 | 888-397-3742 |

| TransUnion | P.O. Box 2000, Chester, PA 19016 | 800-916-8800 |

How to Improve Your Credit Score Before Applying for a Mortgage

Boosting your credit score before applying for a mortgage takes planning and timing. By knowing what steps to take and when, you can ensure your efforts reflect positively on your credit report when lenders review it.

Start about 12 months before applying by pulling your credit reports from all three bureaus through AnnualCreditReport.com. Use this time to check for and dispute any errors, as credit bureaus typically have up to 30 days to investigate discrepancies.

By the 6-to-9-month mark, focus on lowering your revolving credit balances to below 30% of your credit limit - ideally under 10%. Setting up autopay on all accounts can help you maintain a spotless payment history. As Brian Walsh, CFP® and Head of Advice & Planning at SoFi, explains:

"Payment history makes a bigger impact on a person's credit score than anything else - 35%. So the most important rule of credit is this: Don't miss payments."

In the 3-to-6 months leading up to your application, avoid applying for new credit to prevent hard inquiries and keep your debt-to-income ratio stable. Also, resist the urge to close old, unused credit cards. Closing accounts can reduce your available credit and shorten your average account age, which affects 15% of your FICO® Score.

You might also consider requesting a credit limit increase from your current card issuers. If approved, this instantly lowers your utilization ratio - provided your spending doesn’t increase - potentially helping you qualify for better mortgage rates. If you're applying with a co-borrower, remember that lenders often use the lower of the two applicants' middle credit scores, so both parties need to be in strong financial shape.

When to Apply for a Mortgage

Once your credit is in good shape, timing your mortgage application strategically can make a big difference. Jordan Del Palacio, a Mortgage Specialist at Churchill Mortgage, advises:

"For conventional loans, typically a 780 score is the point where you get the best rates. The reason being that from 760 above, the difference in score is not so much about creditworthiness but more about how you play the credit game."

Aiming for a FICO® Score of 780 can help you secure the most favorable rates. When you’re ready to apply, submit all your mortgage applications within a 45-day window. FICO treats multiple mortgage inquiries during this period as a single hard inquiry, allowing you to shop around for the best rates without significantly impacting your score.

Be cautious after pre-approval. Lenders often perform a "credit refresh" just before closing. Taking on new debt - like financing furniture - can jeopardize your loan approval. To avoid surprises, keep your finances stable from application to closing.

Using Financial Tools to Stay on Track

Improving your credit score isn’t just about managing debt - it’s also about keeping a close eye on everyday spending. High credit card balances can sneak up on you, so knowing exactly where your money goes each month is essential.

This is where an app like Monefy can come in handy. Monefy helps you track expenses by category, monitor your income, and set budget limits to prevent overspending. It also offers customizable reminders for payment due dates, helping you maintain a clean payment history. With a 4.7/5 rating from over 283,000 reviews on the App Store and Google Play Store, Monefy is a trusted tool for staying on top of your finances.

The key is developing consistent financial habits - keeping balances low, making on-time payments, and steering clear of new debt for at least 6 to 12 months before applying. These habits not only improve your credit score but also set you up for better mortgage terms.

Conclusion: Building a Credit Profile That Supports Mortgage Readiness

Your credit score plays a major role in determining your mortgage rate. It’s how lenders gauge their risk, which directly impacts the interest rate you’ll pay over the life of your loan. For instance, on a $400,000 mortgage, the difference between a 760 and a 620 FICO® Score could mean paying an extra $433 each month - or over $155,000 in additional interest across a 30-year term. That’s why managing your credit wisely can save you a significant amount of money.

Improving your credit score isn’t magic - it’s about taking specific, calculated steps. Paying down debt, fixing errors on your credit report, and avoiding new credit inquiries in the months leading up to your application can help you qualify for better rates. As Max Slyusarchuk, CEO of AD Mortgage, explains:

"A difference of 20 or 30 FICO points may seem small, but over the life of a mortgage, it can determine whether a borrower pays an extra $20,000 in unnecessary interest."

It’s also important to note that the credit score you see as a consumer might differ from the one lenders use. If you’re applying with a co-borrower, lenders typically go with the lower of the two middle scores. Understanding these details can help you better prepare for the best possible loan terms.

The median FICO® Score for homebuyers reached approximately 736 in early 2026, marking a six-year high. With lender requirements becoming stricter, treating your credit profile as a long-term asset is more important than ever. A strong credit profile doesn’t just help you qualify - it positions you for the most competitive rates available.

<div class="accordion"> <h2 class="accordion-title">Questions? Answers.</h2> <p class="accordion-subtitle">Common questions about credit scores and mortgage rates</p>

<div class="accordion-item">

<div class="accordion-header">

<span>What credit score do I need to get the best mortgage rate?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>For conventional loans, aim for a FICO® Score of 760 or higher. Scores above 780 rarely result in additional savings, so 760 is a practical target for securing the best rates in 2026.</p>

</div>

</div>

<div class="accordion-item">

<div class="accordion-header">

<span>How much can a higher credit score save me on a mortgage?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>The savings can be substantial. On a $400,000 mortgage, the difference between a 760 and a 620 FICO® Score could be as much as $433 per month. Over 30 years, improving your score to the top tier could save between $9,547 and $46,206 in total interest, depending on your state’s home values.</p>

</div>

</div>

<div class="accordion-item">

<div class="accordion-header">

<span>How long does it take to improve a credit score before applying for a mortgage?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>Most experts recommend starting at least 12 months before applying. On average, you can expect to improve your score by around 20 points per year. If you’re within 20 points of a higher pricing tier, waiting 6 to 12 months before locking in a 30-year loan could be worth it financially.</p>

</div>

</div>

<div class="accordion-item">

<div class="accordion-header">

<span>Does checking my credit score hurt my chances of getting a mortgage?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>Checking your own credit score is considered a soft inquiry and doesn’t affect your score. However, when lenders pull your credit during the mortgage application process, it’s a hard inquiry, which might lower your score slightly. That said, FICO treats multiple mortgage-related hard inquiries within a 45-day window as a single inquiry.</p>

</div>

</div>

<div class="accordion-item">

<div class="accordion-header">

<span>What credit score do lenders actually use for mortgage applications?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>Lenders pull scores from all three major credit bureaus and use the median score for qualification. If you’re applying with a co-borrower, they’ll consider the lower of the two median scores. Keep in mind the score you see on consumer apps may not match the one lenders use.</p>

</div>

</div>

</div>