Budgeting helps you manage your money effectively by balancing immediate needs and future goals. A strong budget allocates funds for essentials, reduces unnecessary spending, and ensures progress toward financial stability. Here’s how to approach it:

- Short-term goals (within 1 year): Build an emergency fund ($500–$1,000), pay off credit card debt, or save for holiday travel. These goals provide quick wins and peace of mind.

- Long-term goals (5+ years): Save for retirement (10–15% of income), pay off a mortgage, or fund education. These require consistency and patience.

- Track income and expenses: Use tools like Monefy to categorize spending, identify surplus, and automate savings.

- Allocate wisely: Start with an emergency fund, contribute to retirement (especially if your employer offers a match), and pay off high-interest debt.

Identifying and Defining Financial Goals

Before diving into budgeting, it's crucial to define your financial goals. A vague objective like "save more" doesn't provide a clear path forward. Instead, aim for goals that are specific, measurable, and time-bound. The SMART framework can guide you here. For instance, rather than saying, "I want to save for emergencies", set a concrete target like saving $2,000 over six months for an emergency fund. This kind of clarity turns an abstract idea into a plan you can act on.

"Knowing what you want and putting it in writing is an important first step. But to get where you want to go, you'll need to be more specific." - Rob Williams, Managing Director of Financial Planning, Schwab Center for Financial Research

Once you've outlined your goals, categorize them by timeline. Short-term goals (within one to two years) might include building a starter emergency fund or paying off credit card debt. Medium-term goals (three to ten years) could focus on saving for a home down payment or funding a major renovation. Long-term goals (ten years or more) often center on retirement, college tuition, or paying off a mortgage.

How to Set Realistic Short-Term Goals

Short-term goals lay the groundwork for your financial stability. Start with a basic emergency fund - aim for at least $500 to cover unexpected expenses like car repairs or medical bills. This safety net can help you avoid turning to high-interest credit cards when surprises arise. Notably, 46% of Americans plan to save specifically for emergencies by 2026.

Next, tackle high-interest debt, such as credit card balances. The average American carries about $96,371 in total debt, so reducing this load can free up cash for other priorities. Consider using debt payoff strategies like the "debt avalanche" method, which targets the highest interest rates first, or the "debt snowball" approach, which focuses on paying off smaller balances quickly for a sense of accomplishment. Choose the strategy that keeps you motivated.

Other short-term goals might include saving for holiday travel, handling minor home repairs, or setting aside three to six months' worth of living expenses in your emergency fund. Assign specific targets and deadlines. For example, you could save $150 per month to reach $1,200 for a vacation in eight months.

How to Plan for Long-Term Goals

Long-term goals often require patience and persistence, but they’re essential for securing your financial future. Retirement savings frequently top this list. Experts recommend saving 10% to 15% of your pre-tax income, including any employer match, to build a robust retirement fund. The earlier you start, the more time your money has to grow through compounding.

"Time is your biggest advantage when it comes to long-term financial planning. The earlier you start saving for retirement, the less financial stress you'll face later." - Noah Damsky, Founder, Marina Wealth Advisors

Other long-term goals might include paying off a mortgage, funding a child’s college education (remember, the average student loan balance exceeds $38,000), or growing wealth through investments. Tools like 401(k)s, IRAs, and 529 college savings plans can help you achieve these objectives. Unlike short-term savings, long-term funds can be invested in accounts designed to grow over time.

As you plan, consider how your life stage affects your goals. For example, early-career individuals might focus on building an emergency fund and reducing debt, while those in their 40s and 50s may prioritize estate planning and maximizing retirement contributions. Your priorities may shift over time, but the key is to begin now and stay consistent.

With your goals clearly defined, the next step is to assess your income and expenses to figure out how much you can allocate toward achieving them.

Assessing Income and Tracking Expenses

Getting a clear picture of your after-tax income is the first step toward building a solid budget. This is the amount that actually lands in your bank account after deductions like federal, state, and local taxes, along with FICA taxes (7.65% for most employees). For the 2026 tax year, federal income tax rates range from 10% to 37%, depending on your taxable income. If you contribute to a traditional 401(k) or pay for health insurance through your employer, these pre-tax deductions reduce your taxable income before taxes are calculated.

To figure out how much you can actually budget, start by subtracting pre-tax contributions and mandatory deductions from your gross pay. This gives you your net income, or take-home pay. If you're self-employed, you'll need to take out business expenses and estimated self-employment taxes (15.3% for FICA) from your gross revenue. For those with variable incomes, like freelancers or commission-based workers, it’s smart to use the lowest monthly income from the past 6 to 12 months as a conservative starting point.

Using Tools to Track Income and Expenses

Once you know your net income, tracking your spending is the next step. Budgeting apps make this process much easier by syncing with your bank accounts, categorizing transactions automatically, and handling the math for you. Take Monefy, for example - it helps you track expenses, manage income, and sync data across devices, giving you a clear picture of your spending habits in real time. The app’s automatic categorization feature simplifies sorting your spending into fixed expenses (like rent, insurance, and loan payments) and variable expenses (such as groceries, dining out, and entertainment).

"Understanding of your monthly saving and spending habits allows you to make smart financial decisions that can position you for long-term security." - Morgan Stanley

To stay on top of your spending, track daily expenses and review them weekly. For annual costs like vacations or car registration, divide the total by 12 to include a portion in your monthly budget. Once you’ve mapped out your income and expenses, you can calculate how much you have left to work toward your financial goals.

Identifying Surplus for Goal Allocation

Your surplus is the amount left over after covering all your expenses - both fixed and variable. This is the money you can use to achieve your financial goals. To calculate it, subtract your essential expenses (housing, utilities, groceries, insurance, minimum debt payments) and discretionary spending (entertainment, hobbies, subscriptions) from your net income. For instance, if your monthly net income is $4,500 and your total expenses come to $3,800, you’ll have $700 left to allocate toward savings, debt repayment, or long-term goals like retirement.

One way to make sure your surplus goes where it should is by automating transfers to savings accounts on payday. This “pay yourself first” method ensures that your goals are prioritized before you spend on non-essentials. If you find yourself with no surplus - or even a deficit - take a closer look at your variable expenses to identify areas for cuts. Recurring charges like streaming services, gym memberships, or subscription boxes can often be reduced or eliminated. Even small changes, like cutting back on dining out by $100 a month, can free up cash to help you make progress toward your goals. With your surplus in hand, you’re ready to focus on funding both short- and long-term financial priorities.

Allocating Budget for Short- and Long-Term Goals

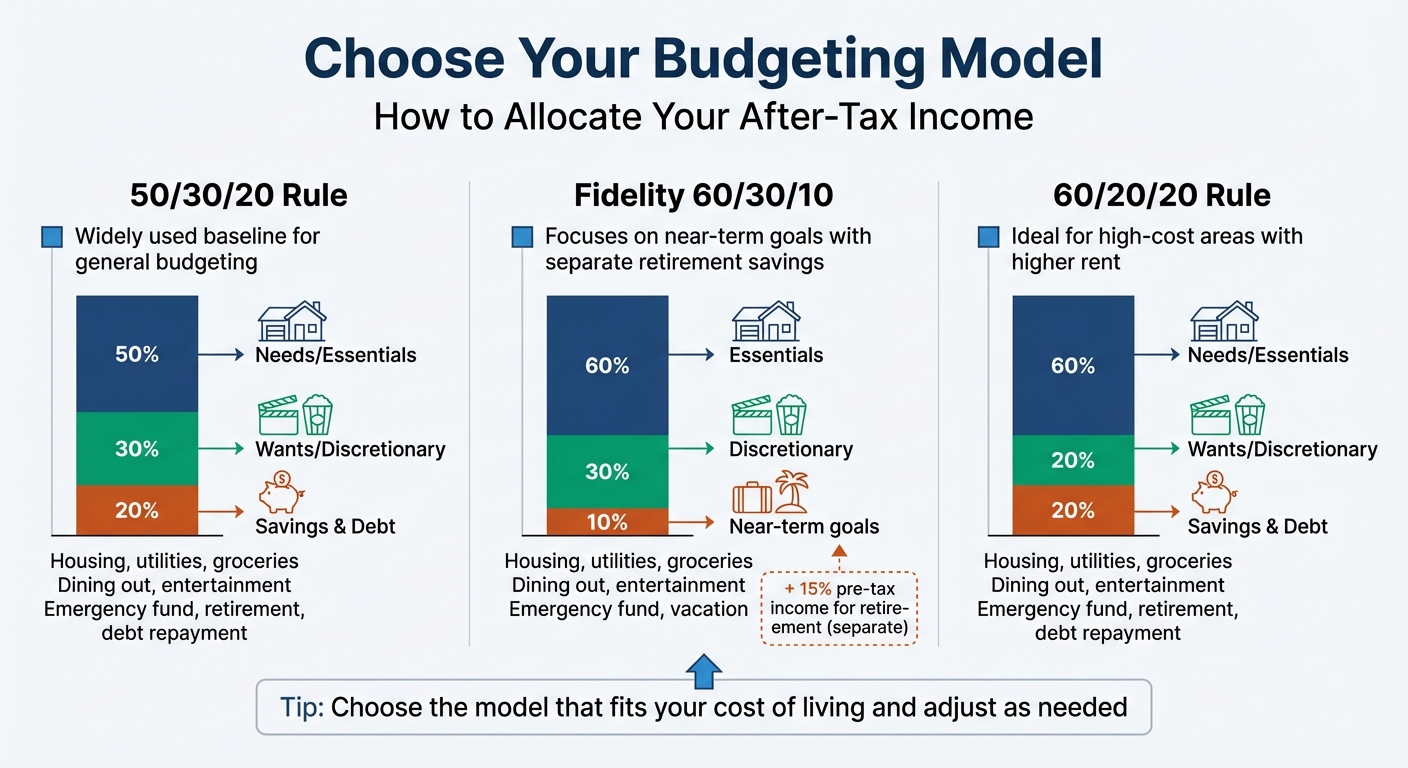

Budgeting Models Comparison: 50/30/20 vs 60/30/10 vs 60/20/20 Rules

Once you've identified your surplus, the next step is to allocate those funds wisely. The goal is to shield yourself from financial setbacks while steadily building wealth over time. Here's a common approach recommended by many financial experts: prioritize essentials first, set up a starter emergency fund, take advantage of your employer's 401(k) match, pay off high-interest debt, build a full emergency fund (enough to cover three to six months of essential expenses), and then focus on long-term retirement savings and other financial goals. This method connects your immediate financial security with your future wealth-building plans.

Prioritizing Emergency Fund and Debt Repayment

Start by creating a small emergency fund of $500 to $1,000 after covering your basic expenses. This buffer can help you handle minor surprises - like a car repair or a medical bill - without resorting to high-interest debt.

Once this starter fund is in place, contribute enough to your 401(k) to receive the full employer match. This is essentially free money and a great way to jumpstart your retirement savings. After that, focus on eliminating high-interest debt, such as credit card balances or payday loans, which often carry interest rates between 18% and 25% or more. In fact, 30% of Americans plan to fully pay off one or more debts by 2026. Once you've tackled high-interest debt, work on building a full emergency fund that can cover three to six months of essential expenses. Keeping this money in a high-yield savings account ensures it's readily available when needed but remains separate from everyday spending.

After securing these financial safety nets, you can start distributing your surplus between immediate needs and future goals.

Balancing Short- and Long-Term Goals

With your emergency fund established and high-interest debt under control, it's time to balance your budget between short- and long-term priorities. A commonly used guideline is the 50/30/20 rule: allocate 50% of your after-tax income to needs (like housing, utilities, and groceries), 30% to wants (such as dining out or entertainment), and 20% to savings and debt repayment. While this framework is a helpful starting point, it's not a one-size-fits-all solution.

"It's helpful to start with a common framework, such as the 50-30-20 rule... It's a good starting point, but you need to evaluate personal circumstances, such as the cost of living in the region you live in, to determine the best allocation for your lifestyle." - Justin Green, Financial Planner and Founder, Assist Financial Planning

For those living in high-cost areas where housing takes up a larger chunk of income, a 60/20/20 split might be more realistic - 60% for needs, 20% for wants, and 20% for savings. Another option is Fidelity's 60/30/10 + 15 guideline, which allocates 60% to essentials, 30% to discretionary spending, and 10% to near-term goals (like an emergency fund or vacation), while separately saving 15% of your pre-tax income for retirement.

| Budgeting Model | Needs/Essentials | Wants/Discretionary | Savings & Debt | Notes |

|---|---|---|---|---|

| 50/30/20 Rule | 50% | 30% | 20% | A widely used baseline for general budgeting |

| Fidelity 60/30/10 | 60% | 30% | 10% | Focuses on near-term goals; assumes 15% pre-tax retirement is separate |

| 60/20/20 Rule | 60% | 20% | 20% | Ideal for high-cost areas with higher rent costs |

Aim to set aside 10%–15% of your pre-tax income for retirement, including any employer match. For example, if you have a $700 monthly surplus, you might allocate $300 to retirement accounts, $200 to short-term goals (like saving for a vacation or a car), and $200 to paying off low-interest debt or padding your savings. Automating these contributions on payday with tools like Monefy can help you stay on track and resist the temptation to spend impulsively.

sbb-itb-02fd20a

Monitoring Progress and Adjusting Plans

Creating a budget is just the beginning; the real work lies in tracking your progress and tweaking your plan as life unfolds. Make it a habit to review your budget monthly, and do a more comprehensive update annually. Changes like a pay raise or surprise expenses can impact your financial plan, so these regular check-ins help you adapt and stay on course. Plus, they give you a chance to break big goals into smaller, more manageable steps.

Setting Milestones and Timelines

Tracking progress becomes much easier when you divide long-term goals into smaller, achievable milestones. For instance, instead of focusing solely on building a large emergency fund, celebrate the smaller wins along the way - like saving $500, then $1,000, and so on. These little victories can keep you motivated and make the journey feel less overwhelming.

"Breaking down big or long-term goals into more manageable intermediate steps... can give you a psychological boost when you reach them." - Bank of America

To stay organized, apply the SMART criteria to each milestone: make them Specific, Measurable, Attainable, Relevant, and Time-bound. For example, set a goal like "save $300 per month for my 401(k) over the next year." Clearly defined milestones like this not only hold you accountable but also help you decide where every dollar should go.

| Milestone | Timeline at $200/month | Timeline at $500/month |

|---|---|---|

| Starter Fund ($500) | 2.5 months | 1 month |

| Foundation ($1,000) | 5 months | 2 months |

| Basic Protection ($2,500) | 12.5 months | 5 months |

| Full Coverage ($5,000+) | 25+ months | 10+ months |

Using Monefy for Continuous Tracking

Keeping tabs on your progress is crucial to ensure you're meeting both short- and long-term goals. Tools like Monefy make this process simple by offering visual progress indicators and goal-specific categories. For example, you can create separate categories like "Emergency Fund" or "Down Payment" and watch the progress bars fill as you contribute. The app even lets you add notes to transactions - like "Tax refund allocation" or "Auto transfer" - so you can track what strategies are working best.

One effective strategy is setting up automatic transfers to your savings or investment accounts right after payday. This "pay yourself first" approach ensures consistent progress before you’re tempted by discretionary spending. Monefy also syncs across multiple devices, so you can monitor your goals anytime, anywhere. At the end of each month, compare your balances to your targets, check if you’ve been contributing regularly, and adjust your budget as needed. If you notice seasonal spending spikes - like during the holidays - you can plan ahead and tweak your monthly goals to stay on track year-round.

Conclusion

As your life changes, so should your financial plan. A well-thought-out plan strikes a balance between meeting today’s needs and working toward tomorrow’s goals. Justin Green, Financial Planner and Founder of Assist Financial Planning, highlights this perfectly:

"The most important part is self-reflection and being intentional about how you use your money. If you have a clear vision for how you want to live your life now and in the future, then you can reverse engineer the math."

It’s all about finding that balance - managing your current expenses while preparing for what’s ahead. For instance, with 46% of Americans aiming to save for emergencies by 2026 and 30% planning to eliminate at least one debt by then, having a system to keep yourself accountable is critical. At the same time, your plan needs to be flexible enough to adapt to life’s inevitable surprises.

That’s where tools like Monefy come in. By simplifying expense tracking and keeping your financial goals front and center, it helps you stay on course - whether you're building an emergency fund or focusing on retirement savings. Plus, with real-time tracking and multi-device syncing, you can monitor your progress anytime, ensuring you catch potential issues before they throw you off track.

FAQs

How can I budget effectively for both short-term and long-term financial goals?

To manage both short-term and long-term financial goals effectively, start by getting a clear picture of your income, spending habits, and savings. A popular strategy to guide your budgeting is the 60/30/10+15 rule: allocate roughly 60% of your take-home pay to essentials, 30% to discretionary spending, 10% to short-term goals or an emergency fund, and aim to save 15% of your pre-tax income for long-term objectives like retirement.

The first step is to list all your income sources and categorize your expenses. Then, define your goals. Short-term goals might include building an emergency fund or planning a vacation, while long-term goals could involve saving for retirement or buying a home. Assign a specific percentage or dollar amount to each goal, and revisit your budget monthly to make adjustments as your priorities shift. For instance, once you’ve achieved a short-term goal, you can redirect those funds toward your long-term savings.

Using budgeting apps like Monefy can make this process easier. These tools allow you to create goal categories, track your contributions, and visualize your progress, keeping you organized and motivated. With consistent tracking and periodic adjustments, you can strike a balance between meeting today’s needs and securing your financial future.

How can I effectively track and manage my budget for short- and long-term goals?

Managing your budget well starts with organizing your income into distinct categories: essentials (like rent and utilities), discretionary spending (such as dining out or entertainment), short-term goals (like vacations or new gadgets), and long-term goals (think retirement or emergency savings). By assigning specific dollar amounts to each category, you can set achievable targets that align with your financial priorities.

To simplify the process, consider using a personal finance app like Monefy. These tools let you track every expense, sort spending into categories, and see your progress toward savings goals with clear visuals. Automating savings transfers or recurring payments can also keep things consistent and reduce the hassle of manual budgeting.

Make it a habit to log expenses as they occur. Regularly reviewing your budget helps you spot trends, tweak categories when needed, and confirm that your financial goals match your income. These practices can give you better control over both your immediate needs and future plans.

What should I do if my financial situation changes unexpectedly?

If you face an unexpected financial setback, like losing your job or dealing with a hefty medical bill, the first step is to evaluate your cash flow. Start by listing all your current sources of income. Then, subtract essential expenses such as rent or mortgage payments, utilities, groceries, and the minimum payments on any debts. Take a close look at discretionary expenses - things like dining out, streaming services, or other subscriptions - and identify areas where you can cut back or pause spending for the time being.

Once you've done that, rework your budget to focus on covering necessities and building up an emergency fund. A practical guideline is to allocate about 60% of your income to essential expenses, 30% to flexible spending, and 10% to savings. If your emergency fund doesn’t yet cover three to six months of expenses, make it a priority to grow it. This will give you a safety net for any future financial surprises.

Lastly, make sure to track your progress so you can adapt as needed. Budgeting tools like Monefy can help you set up a category for your emergency fund, monitor your savings contributions, and keep tabs on adjustments like cutting back on non-essential spending. Regularly reviewing your budget will help ensure it stays in line with your changing circumstances, keeping you on the path to financial stability.