When disasters strike, the financial impact can be overwhelming. From unexpected costs like temporary housing and emergency supplies to job interruptions and limited banking access, many households struggle to recover. This guide breaks down practical steps to help you prepare financially for emergencies and recover faster when the unexpected happens.

Key Steps to Financial Preparedness:

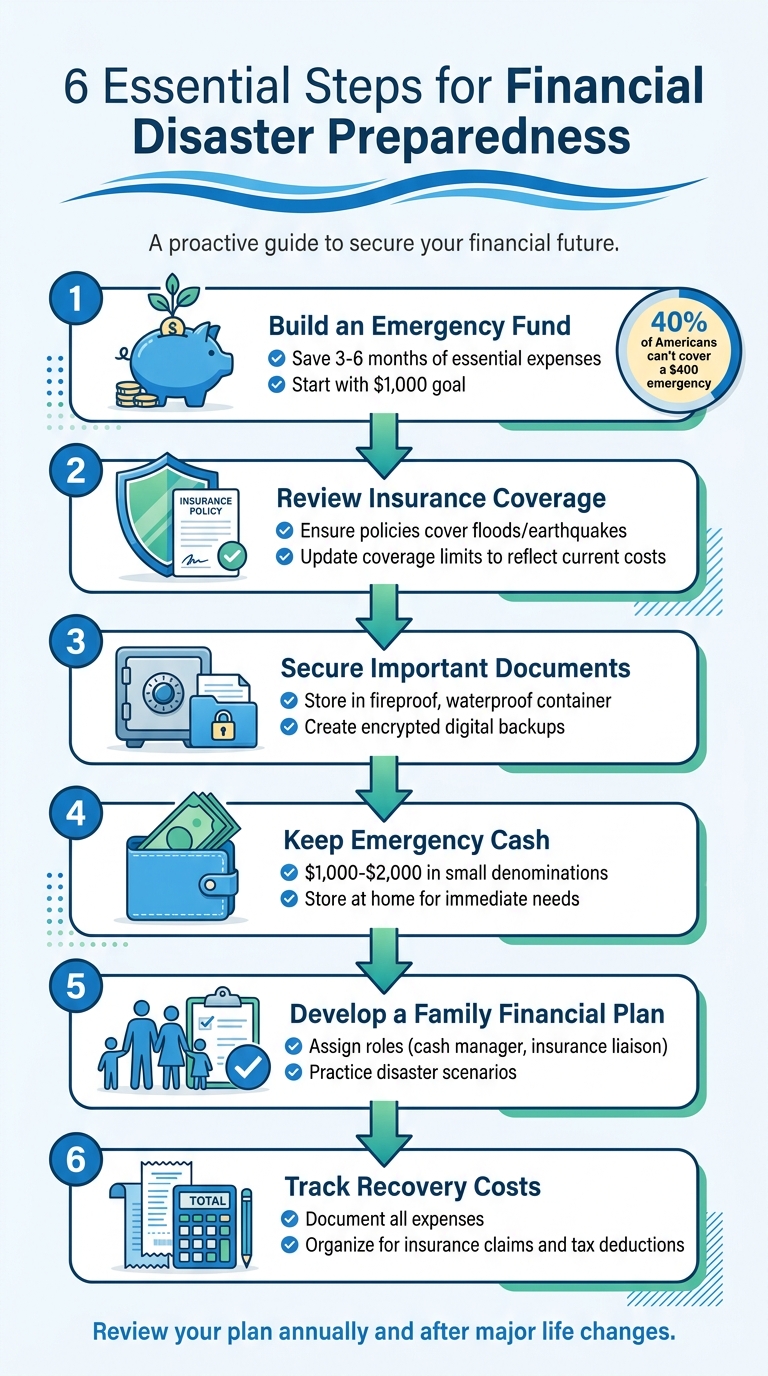

- Build an Emergency Fund: Save 3-6 months of essential expenses; start with a $1,000 goal.

- Review Insurance Coverage: Ensure policies cover risks like floods or earthquakes; update coverage limits to reflect current costs.

- Secure Important Documents: Store key records (IDs, insurance policies, tax returns) in a fireproof, waterproof container and create encrypted digital backups.

- Keep Emergency Cash: Have $1,000–$2,000 in small denominations at home for immediate needs during power outages.

- Develop a Family Financial Plan: Assign roles (e.g., who manages cash or insurance claims) and practice scenarios to ensure readiness.

- Track Recovery Costs: Document and organize expenses for insurance claims and tax deductions.

By staying organized and proactive, you can minimize financial stress during disasters. Regularly update your plan, review insurance policies, and maintain emergency savings to stay prepared. Tools like Monefy can simplify budgeting and tracking progress toward your financial goals.

6 Essential Steps for Financial Disaster Preparedness

Build an Emergency Fund

Once you've handled the basics, it's time to strengthen your financial safety net by building an emergency fund. Think of this fund as your financial shield when life throws unexpected challenges your way. With nearly 40% of Americans unable to cover a $400 emergency without borrowing, a single surprise expense can lead to financial trouble. An emergency fund ensures you can handle essential costs without resorting to credit cards. It's a critical step that works alongside insurance, document security, and recovery plans to create a well-rounded disaster preparedness strategy.

Set Savings Goals

Start by keeping track of your expenses for a month to distinguish between "needs" and "wants." Your emergency fund should focus solely on covering essential monthly costs - things like rent, utilities, and groceries. Cut out non-essentials like dining out or streaming subscriptions while building this fund.

The size of your emergency fund depends on your household's financial stability. If you have a steady, dual-income household, aim to save enough for 3 months of essential expenses. If you're self-employed, work seasonally, or are the sole earner, aim for 6 months. Break this big goal into smaller, more manageable steps: save $500 as a starting buffer, then work toward $1,000 to avoid falling into debt, and eventually save for 1 month, then 3–6 months of expenses.

| Monthly Savings | Time to $1,000 Starter Fund | Time to $10,000 Full Fund |

|---|---|---|

| $100 | 10 months | 8+ years |

| $300 | 3.5 months | 3 years |

| $500 | 2 months | 20 months |

| $1,000 | 1 month | 10 months |

A solid emergency fund is a key part of staying financially secure during tough times.

Use Tools to Track Progress

Staying motivated can be tough, especially when your savings goal feels far away. Apps like Monefy (https://monefy.com) can help by providing visual progress bars and target dates, making your goals feel more achievable. Automate your savings by setting up transfers from your checking account to your savings right after payday. This "pay-yourself-first" strategy eliminates the need for constant self-discipline.

Check in on your progress every month and adjust your contributions if needed. If saving aggressively feels overwhelming, try the 1% method: start by saving 1% of each paycheck and increase it by 1% every month. You can also use windfalls like tax refunds (averaging $2,800 to $3,000) or work bonuses to boost your fund.

Choose a High-Yield Savings Account

To make your emergency fund work harder for you, keep it in an FDIC-insured high-yield savings account. These accounts protect deposits up to $250,000 per depositor and, as of 2026, offer interest rates between 4.0% and 5.0% APY - much higher than the 0.45% to 0.65% offered by traditional banks. For example, this difference could save you around $440 in interest on a $2,000 repair over two years.

Look for an account with no monthly fees or minimum balance requirements, and make sure you can access your funds within 1–2 business days. Keeping your emergency fund at a different bank than your main checking account can also discourage impulse withdrawals. Some high-yield accounts even allow you to create sub-accounts or "buckets" for specific needs like car repairs or medical expenses.

"An emergency fund allows individuals and families to cover these urgent needs without relying on credit or loans - helping them navigate the first critical days of recovery with greater stability and less stress." - Walter English, Deputy Coordinator of Emergency Management for Fairfax, Virginia

Finally, for disasters that might involve power outages, keep a small amount of cash at home in a waterproof and fireproof container. This way, you'll still have access to money if ATMs or card systems are down.

This step completes your financial safety net, setting the stage to secure other important documents next.

sbb-itb-02fd20a

Review and Update Insurance Coverage

Having an emergency fund is crucial, but insurance acts as a safety net for your assets, protecting them from major losses that could drain your savings in one fell swoop. Just as your emergency fund ensures steady cash flow during tough times, keeping your insurance policies up to date guards against financial ruin caused by disasters. Making sure your coverage matches your current needs is just as important as building that emergency fund.

Verify Policy Coverage

Start by reviewing your current homeowners or renters insurance policy, paying close attention to the exclusions section. Most HO-3 policies cover your home's structure against a wide range of risks, except for those explicitly excluded - like floods, earthquakes, landslides, and sinkholes. However, personal belongings are often only protected under more limited "named perils" coverage. If you have an HO-2 policy, it’s even more restrictive, covering only the specific disasters listed in the policy. For instance, if fire or wind damage isn’t mentioned, you won’t be eligible for a payout.

If you live in a hurricane-prone area, confirm whether your policy includes wind damage - this is a critical detail. Renters, on the other hand, should ensure they have their own insurance policy, as a landlord’s coverage only protects the structure of the building, not your personal belongings or temporary housing needs.

Understand Deductibles and Limits

Take a close look at the details of your policy, as these dictate how much you’ll receive in the event of a disaster. Dwelling coverage should reflect the cost to rebuild your home from the ground up, not its current market value. For example, while your home might have a market value of $300,000, rebuilding it could cost $400,000 due to rising construction expenses.

Personal property coverage often includes sub-limits for certain categories. For instance, while your policy might cover $100,000 in total belongings, it might cap jewelry coverage at $2,500, electronics at $5,000, or cash stored at home at $500. Additionally, check your "loss of use" coverage, which helps cover temporary housing and meal costs if your home becomes uninhabitable - this can be a lifesaver during prolonged repairs.

It’s also important to understand the difference between replacement cost coverage and actual cash value coverage. Replacement cost coverage reimburses you for new items at today’s prices, while actual cash value coverage only pays for the depreciated value of your items. Finally, make sure your deductible is reasonable compared to your emergency savings. A high deductible might lower your premiums but could leave you in a tough spot if you don’t have enough cash set aside.

Consider Additional Policies

Depending on where you live, you might need extra coverage beyond what a standard policy offers. For example, flood insurance, which is usually excluded from standard policies, can be purchased through the National Flood Insurance Program (NFIP). The NFIP even reimburses up to $1,000 for supplies like sandbags, lumber, and tarps when flooding is imminent.

If you’re in an area prone to earthquakes, you’ll need a separate earthquake insurance policy or endorsement. Additionally, it’s a good idea to check your insurer’s financial health using ratings from agencies like A.M. Best, Fitch, Moody’s, or S&P Global. This ensures they’ll be able to pay out claims after a major disaster. Once your insurance is in order, you can turn your attention to organizing your financial documents.

Secure Financial Documents

After sorting out your insurance, the next step is ensuring you can prove ownership of assets and access your accounts during an emergency. In 2024, the U.S. experienced 27 weather and climate disasters, each causing over $1 billion in damages. Having your financial documents organized and easily accessible can make a huge difference - helping you get assistance quickly instead of waiting weeks to replace lost paperwork. This preparation becomes critical when other systems fail.

"Having access to personal financial, insurance, medical and other records is crucial for starting the recovery process quickly and efficiently." – Ready.gov

Create a Document Kit

Assemble a waterproof, fireproof, and portable "financial go bag" that you can grab at a moment's notice. This kit should include copies (or certified copies if originals are stored elsewhere) of key documents like:

- Driver's licenses, passports, Social Security cards, and birth certificates

- Recent bank statements and tax returns from the last two years

- Mortgage or rent payment records

- Current insurance policies, including your agent's contact information

Don’t overlook medical records. Include health insurance cards (e.g., Medicare, Medicaid, or VA cards), a list of medications with dosages, allergy details, and your physician's contact information. Add legal documents such as wills, trusts, and powers of attorney. For household inventory, include receipts and photos of valuable items. If you store originals in a bank safe deposit box, remember these boxes are not waterproof - place documents in waterproof bags before storing them. And since banks might be inaccessible during a disaster, keep physical copies at home.

Also, add copies of the front and back of your credit and debit cards, along with a small stash of cash in $1, $5, $10, and $20 denominations. In power outages, ATMs and card readers may not work, making cash essential for immediate needs.

Once your physical documents are secure, don’t forget to set up digital backups for added protection.

Set Up Digital Backups

Physical documents are vulnerable to loss, theft, or damage, so digital backups are a must. Scan or photograph all essential documents and store encrypted copies in secure cloud storage with multi-factor authentication. Adding a second verification step, like a code sent to your phone, provides an extra layer of security.

"Encrypt sensitive documents and set your electronic device security to require a password, your thumbprint, or facial recognition for additional safety." – FDIC

Additionally, keep a second encrypted backup on an external drive stored in a fireproof, waterproof container at an offsite location. Password-protect files containing sensitive data like Social Security numbers or account details. For added preparedness, use your smartphone to record a video walkthrough of your home. Document serial numbers on electronics, details about furniture, and the condition of items - this can be invaluable when filing insurance claims.

Download your bank's mobile app to manage bill payments, transfer funds, and access account information remotely, or download a personal finance app to track expenses during recovery. This ensures you can handle finances even if your local branch is closed or your mailbox is compromised. Lastly, switch federal benefits like Social Security to direct deposit. This eliminates reliance on mail delivery and ensures uninterrupted access to your funds, even during postal service disruptions.

Create Digital and Cash Backups

Backing up your financial resources with digital records and emergency cash can make a huge difference during extended outages. When cloud storage or mobile banking services go down, having these backups ensures you’re not left stranded.

Photograph Valuables and Store Receipts

If you ever need to file an insurance claim, you'll need proof of ownership and value for your belongings. Start by recording a video walkthrough of your home, focusing on high-value items like electronics, furniture, jewelry, and appliances. Be sure to document serial numbers and note the condition of each item.

Next, scan or photograph receipts and appraisals for your valuables. Save these digital copies in password-protected files on an external flash drive, which should be stored offsite. Meanwhile, keep the original receipts in your fireproof and waterproof document kit. Regularly update your inventory - whether it’s after a big purchase like a new laptop or a home renovation. Aim to review and refresh this list at least once a year.

"Having insurance for your home or business property is the best way to make sure you will have the necessary financial resources to help you repair, rebuild or replace whatever is damaged. Document and insure your property now." – Ready.gov

With your inventory safely stored, you’ll also want to ensure you have quick access to cash for emergencies.

Keep Emergency Cash

When card readers and ATMs stop working, cash becomes a lifeline. Store between $1,000 and $2,000 in small denominations - $1s, $5s, $10s, and $20s - in a waterproof and fireproof container at home. Smaller bills are crucial since businesses might not have change during a crisis. This cash will cover essentials like food, fuel, and other supplies.

"Disasters can disrupt income, limit access to banking services, and create unexpected expenses like hotel stays, gas for evacuation, or replacing essential supplies." – Walter English, Deputy Coordinator of Emergency Management

Keep about $200 to $300 of this cash in your go-bag for quick evacuations. The rest should remain in a secure but easily accessible spot at home. This stash is meant to cover immediate needs in the first few days of an emergency, not to replace your full emergency savings.

Enable Multi-Device Syncing

To strengthen your financial preparedness, ensure your digital records are accessible across multiple devices. This way, even if one device fails, you can still retrieve your information. Many financial apps offer multi-device syncing, allowing you to manage accounts, track expenses, and monitor savings goals from a phone, tablet, or laptop.

For example, Monefy includes multi-device syncing in its Pro Plan, helping you stay on top of your finances during emergencies. Use your bank’s mobile app to handle bill payments and transfers remotely, even if local branches are closed.

To protect your digital records, enable multi-factor authentication and biometric security on all devices. Install antivirus software on both your smartphone and computer to prevent malware from compromising your financial data. These precautions ensure your finances stay secure and accessible, no matter the situation.

Develop a Family Financial Response Plan

Having a clear family financial response plan in place can make all the difference when disasters strike. It works hand in hand with your emergency fund and organized documents to ensure your family can recover quickly. Without assigned roles, essential tasks - like filing insurance claims or accessing emergency funds - could be overlooked.

Assign Financial Roles

Start by creating a financial chain of command that functions even if the primary money manager is unavailable. Assign specific responsibilities to individuals:

- Cash Custodian: This person carries and secures emergency cash during an evacuation.

- Insurance and Claims Liaison: Manages insurance policy details and handles the claims process.

- Creditor and Utility Coordinator: Contacts banks, credit card companies, mortgage servicers, and utility providers to flag accounts or request payment deferrals.

Make sure at least one trusted adult can handle routine financial tasks, like paying the mortgage or accessing online banking. This avoids a "single point of failure" in your plan. Even teenagers can be included in age-appropriate ways - such as learning where the financial binder is stored or how to contact the bank in an emergency.

"If you are the only person in your household who understands the plan, you have created a single point of failure." – Millions Pro

Store login credentials for banking and insurance portals in a secure password manager that at least two trusted adults can access. This ensures continuity if one person is unavailable. Finally, compile a detailed emergency contact list to support these roles.

Maintain Emergency Contact Lists

Keep both physical and encrypted digital copies of your emergency contact list. Include account numbers, policy details, and official website URLs for easy access. Here's a breakdown of what to include:

| Contact Category | Specific Entities to Include |

|---|---|

| Financial | Banks, credit unions, brokerage firms, financial advisors, credit card issuers |

| Insurance | Agents for homeowners/renters, auto, life, and health insurance |

| Housing & Utilities | Landlords, mortgage representatives, utility service providers |

| Medical | Primary doctors, specialists, dentists, pharmacies |

| Legal & Government | Lawyers, tax professionals, social security/disability offices |

Including official website URLs is crucial since online account management may be your only option if physical branches are closed. Pair these details with account numbers and policy information to make re-establishing accounts easier if physical cards or documents are lost.

"Make sure you store important phone numbers somewhere besides just your cell phone." – FEMA

Review and update your contact list every six months to reflect changes like a new job, a move, or family growth.

Practice Financial Scenarios

Once roles and contacts are set, practice your plan to ensure your family is ready for real-life situations. Conduct "financial fire drills" to simulate the most likely disruptions: sudden job loss, a major medical event, or a natural disaster.

During these drills:

- Show trusted adults where account numbers, login credentials, and insurance policies are stored.

- Test access to digital and physical backups, such as encrypted cloud folders or fireproof safes.

- Practice retrieving cash, securing documents, and managing accounts if the primary manager is unavailable.

"A written family financial emergency plan removes the guesswork during the worst possible moments. Instead of scrambling to figure out which bills to pay first... you already have a prioritized action list." – Millions Pro

Schedule these drills every six months to keep everyone prepared. Use this time to confirm that your insurance policies cover local risks like flooding or earthquakes, which are often excluded from standard coverage. With nearly 37% of American adults struggling to cover an unexpected $400 expense, having a well-practiced plan can provide much-needed stability during tough times.

Inventory Household Assets

Creating a detailed inventory of your household belongings can make insurance claims much easier. Studies show that most people forget 30–50% of their possessions when trying to recall them from memory. The average American household has between $100,000 and $300,000 worth of personal property, and without a proper inventory, much of that value could go unclaimed after events like fires, floods, or theft. This process is a vital step to ensure smoother insurance claims and recovery efforts.

Document and Categorize Valuables

Start by documenting items worth $50 or more individually. Include key details like descriptions, purchase dates, estimated values, brands, models, serial numbers, and conditions. For smaller items - like clothing, kitchen utensils, or linens - group them into categories and assign an overall value (e.g., "Men's clothing - $2,000").

A practical way to tackle this is the "One Room Per Day" method. Dedicate 20–30 minutes to each room, moving systematically clockwise from the door. Open closets, drawers, and cabinets as you go. Take photos of valuable items and record a narrated video walkthrough of each room, mentioning the contents. Don’t overlook items that might seem minor but add up in value, such as spice collections, holiday decorations, or freezer contents - a well-stocked freezer alone can be worth $500–$1,000.

"The best inventory system is one you maintain. A perfect spreadsheet you abandon after two rooms is worth less than a simple app list you keep current." – Matt, Intellist

For high-value items (over $500), gather proof of purchase like receipts, bank statements, or appraisals. This documentation can speed up claims processing. Also, include details about your home’s design, like paint colors or tile types, to help restore it to its original state after a major loss. Store digital copies of your inventory in cloud services like Google Drive, iCloud, or Dropbox, and keep physical copies in a safe deposit box to protect them from disasters.

Estimate Replacement Costs

Assigning replacement values to your belongings can help insurance adjusters process claims more efficiently. Check whether your policy covers Replacement Cost (the price to replace an item with a new one) or Actual Cash Value (the depreciated value at the time of loss), as this determines how you should document the worth of your items. Policies that cover replacement costs often require detailed information, such as model and serial numbers, to ensure accurate replacements.

Be mindful of policy sub-limits for specific categories. For instance, jewelry may have a $5,000 limit, and high-value items might need additional endorsements to receive full coverage. Clothing is another commonly under-reported category, with many households owning between $5,000 and $15,000 or more worth of apparel.

A thorough inventory not only aids in insurance claims but also complements other financial preparedness steps, like securing important documents.

Update Inventory Regularly

Keeping your inventory up to date is just as important as creating it. An outdated list can be nearly as ineffective as having no inventory at all. Schedule a room-by-room walkthrough at least once a year to update values and ensure your documentation reflects your current possessions. Align this review with your annual insurance policy renewal to confirm your coverage still meets your needs.

For significant purchases, document high-value items (typically those over $200) immediately while details and receipts are fresh. Take photos of receipts for items worth $500 or more and upload them right away. To stay on top of things, set calendar reminders for January and July to do quick six-month updates. These can be as simple as a visual sweep to add new acquisitions and remove items you no longer own.

If updating a written inventory feels overwhelming, consider recording a video walkthrough of your home, narrating any changes since your last update. For long-term storage, label boxes with NFC tags to access a digital inventory instantly. Tools like Monefy’s budgeting app (Monefy) can also help you track updates and stay organized with your financial planning.

Plan for Post-Disaster Financial Recovery

After a disaster, managing your finances becomes one of the most critical steps toward recovery. Beyond securing your emergency fund, updating insurance, and safeguarding important documents, having a clear financial recovery plan can ease the transition back to normalcy. Knowing how to access aid, track expenses, and maintain business operations can make all the difference.

Understand Financial Aid Options

Several federal programs are available to help disaster survivors. FEMA's Individuals and Households Program (IHP) can assist with essential needs not covered by insurance, such as temporary housing, personal property replacement, transportation, and medical expenses. You can apply for this assistance through DisasterAssistance.gov or by calling 1-800-621-3362.

If FEMA aid and insurance payouts don't cover all your losses, the Small Business Administration (SBA) offers low-interest disaster loans. These loans are available to homeowners, renters, and businesses to help repair or replace property and cover operational costs. To apply, call 1-800-659-2955 or visit a Disaster Recovery Center near you (use the DRC Locator on FEMA's website).

The IRS also provides tax relief for disaster survivors, including options to claim casualty losses or receive expedited refunds. For more information, contact the IRS at 1-800-829-1040. Additionally, Disaster Unemployment Assistance (DUA) offers benefits to individuals - including self-employed workers - who lose their jobs due to a disaster.

Here’s a quick reference for key resources:

| Resource Type | Organization | Contact Information |

|---|---|---|

| Federal Aid | FEMA | DisasterAssistance.gov or 1-800-621-3362 |

| Low-Interest Loans | SBA | 1-800-659-2955 |

| Tax Relief | IRS | 1-800-829-1040 |

| Unemployment | Dept. of Labor | State or Territorial Workforce Agencies |

| Crisis Counseling | SAMHSA | 1-800-985-5990 (Call or Text) |

| Legal Aid | ABA Young Lawyers | Visit the Young Lawyer's Division website |

Federal aid is designed to cover only what insurance does not. For survivors needing legal assistance with insurance claims, FEMA appeals, or contractor disputes, Disaster Legal Services (DLS) offers free help to low-income individuals. If the stress of recovery feels overwhelming, the Disaster Distress Helpline provides free, confidential mental health support in multiple languages at 1-800-985-5990.

Once you’ve secured aid, make sure to track every recovery-related expense for reimbursement and tax purposes.

Track Recovery Expenses

Keeping detailed records of all recovery expenses is essential. Document damages with photos, list lost items, and save receipts for every cost incurred. These records are crucial for insurance claims and tax deductions.

"Keep receipts for all additional expenses that you may incur such as lodging, repairs or other supplies." – Red Cross

Hold onto receipts for temporary housing, emergency repairs, food, transportation, and essential purchases. Create a dedicated file for these documents, and make copies of everything you submit to insurers or government agencies. If you’ve lost original financial documents, contact your bank or credit card providers for past statements, or use the IRS "Get Transcript" service to retrieve your tax records for free.

Apps like Monefy can simplify expense tracking. Use it to monitor recovery costs, insurance payouts, and your overall budget. Its multi-device syncing feature ensures access to your financial records even if your primary device is unavailable. Setting up specific categories - like temporary housing, repairs, and replacement items - can make it easier to organize reports for claims and deductions.

Prioritize essential payments, such as insurance premiums and housing costs, to maintain coverage and security. If your home is uninhabitable, notify utility providers immediately to pause billing. For other bills, like car loans or credit cards, contact creditors before due dates; many may offer payment deferrals or waive late fees.

For business owners, having a continuity plan is vital to navigate post-disaster challenges.

Prepare Business Continuity Plans

Small business owners often face additional hurdles after a disaster. Beyond personal recovery, maintaining operations and cash flow is key to long-term stability. A business continuity plan can help you outline how to keep essential functions running if your physical location is affected. This might include securing alternative workspaces, backing up customer data, and establishing communication protocols with employees and clients.

The SBA provides disaster loans specifically for businesses to cover operating costs, payroll, and equipment replacement. Apply early, as processing times can take a while. If insurance doesn’t fully cover business losses, these loans can help you stay afloat. Non-profit organizations like Operation Hope (1-888-387-4673) and Project Porchlight (1-877-833-1742) also offer financial counseling to help manage budgets and negotiate with creditors during recovery.

Keep detailed records of all business-related recovery expenses, such as lost inventory, damaged equipment, and revenue losses. These records can support tax deductions and may qualify you for additional aid, including Disaster Unemployment Assistance for self-employed individuals who’ve lost income.

Maintain and Test Your Preparedness Kit

Creating a financial disaster preparedness plan is just the first step - keeping it up to date is what ensures its effectiveness. Life changes, fluctuating insurance policies, and increasing costs can quickly make last year’s plan outdated. For instance, in 2024, the United States faced 27 weather-related disaster events, each causing over $1 billion in damages. With disasters becoming more frequent and expensive, regularly updating your preparedness kit is more of a necessity than ever. Routine maintenance helps ensure your plan keeps pace with your financial needs.

Schedule Routine Reviews

Your financial disaster plan needs regular attention - at least annually, though quarterly reviews are even better. Tie these reviews to key dates, like tax season (by April 15) or insurance renewal periods. During each review, reassess your emergency cash reserves to account for inflation and any changes in your household situation. Major life events, such as getting married, having children, or changing jobs, should trigger an immediate review of your plan.

"Financial preparedness isn't something you set once and forget. Circumstances change, insurance terms evolve, and costs rise." – Landsberg Bennett

Make sure your insurance coverage reflects the current replacement costs for your home and possessions. Policies written five years ago may no longer be sufficient due to inflation and supply chain challenges. Don’t forget to check whether you need separate policies for risks like floods or earthquakes, as these are not typically covered by standard homeowners insurance. Finally, update beneficiaries on wills, trusts, and powers of attorney to avoid legal complications that could delay access to funds in an emergency.

Simulate Disaster Scenarios

Testing your plan with simulations can expose weaknesses that might not be obvious during a simple review. Start by identifying the disasters most likely to affect your area - such as hurricanes, wildfires, or earthquakes - and think through how each could disrupt your finances and daily life. Assign specific roles within your family, like who will handle emergency cash, contact the insurance company, or access digital backups.

"We start with a baseline assessment and then add different scenarios to model out the level of potential disruption to your life and finances in the event of a natural disaster or other catastrophic event." – Min Yoo, Senior Wealth Strategist, U.S. Bank Private Wealth Management

Practice scenarios where the primary financial decision-maker is unavailable. Ensure someone else knows how to access your cloud storage or use secondary devices to retrieve important files. Try logging into your bank’s mobile app from a different device to simulate losing your phone or computer. Everyone in your household should know where emergency cash is stored and who is responsible for managing it. Once you’ve confirmed your plan works under simulated conditions, use financial tools to continue monitoring and adjusting your preparedness.

Use Financial Tools

Apps like Monefy can help you track your progress toward building an emergency fund and adjust budget categories as your needs change. Its multi-device syncing feature ensures access to your financial records even if your primary device is lost - critical during a disaster when you might need to verify account balances or review spending history.

Set up dedicated expense categories for disaster-related costs, such as insurance premiums, emergency supplies, and document storage fees. This makes it easier to monitor your preparedness spending and identify areas for improvement. Use Monefy’s tracking features to maintain the recommended six months of liquid savings.

Additionally, download the Emergency Financial First Aid Kit (EFFAK) from FEMA and Operation HOPE. This resource includes checklists and forms to help you organize your financial information. The FEMA mobile app can also send real-time disaster alerts, prompting you to review your preparedness kit as needed. Finally, switch to direct deposit for Social Security and other federal benefits by calling 800-333-1795 to avoid mail disruptions during emergencies.

Conclusion

This checklist has broken down key steps - from building emergency funds to safeguarding important documents - to help you stay prepared for financial challenges during disasters. Being ready isn't a one-time task; it’s an ongoing effort that directly affects how quickly you bounce back. For instance, disaster-related losses in Florida skyrocketed between 1980 and 2024, highlighting why preparation matters.

"Your financial readiness often determines how fast you recover after a disaster." – Landsberg Bennett

The essentials? Build an emergency fund, confirm your insurance coverage is adequate, secure critical documents, and keep some cash on hand. But here’s the catch: planning is just the first step. Regular reviews are crucial to ensure your plan stays relevant as life changes, costs rise, or insurance policies evolve. Aim to update your plan annually - perhaps during tax season (by April 15) or when renewing insurance. And don’t forget to reassess after major life events like moving, getting married, or welcoming a new family member.

Tools like Monefy can simplify tracking your emergency fund and organizing financial records. With its multi-device syncing, you’ll have access to your financial data even if your primary device is lost - an invaluable feature during emergencies. By combining regular updates with tools like Monefy, you’ll build the financial resilience needed to recover faster after a disaster.

<div class="accordion"> <h2 class="accordion-title">Questions? Answers.</h2> <p class="accordion-subtitle">Common questions about financial disaster preparedness</p>

<div class="accordion-item">

<div class="accordion-header">

<span>How much money should I keep in my emergency fund for disasters?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>Financial experts suggest having an emergency fund that covers 3 to 6 months of your expenses. Additionally, given the rise in disaster occurrences, consider setting aside two weeks' worth of immediate expenses - like lodging, food, and gas - in a separate, easily accessible account. This ensures you have quick access to cash while waiting for insurance claims or disaster relief to process.</p>

</div>

</div>

<div class="accordion-item">

<div class="accordion-header">

<span>What important documents should I include in my disaster preparedness kit?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>Your kit should include copies of key documents such as driver's licenses, passports, Social Security cards, insurance policies, bank account details, medical records, property deeds or leases, birth and marriage certificates, wills, powers of attorney, and tax returns. Keep physical copies in a fireproof, waterproof container, and store encrypted digital backups in secure cloud storage accessible from multiple devices.</p>

</div>

</div>

<div class="accordion-item">

<div class="accordion-header">

<span>Does homeowners insurance cover all types of natural disasters?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>Not always. Standard homeowners insurance often excludes flood and earthquake damage, which typically require separate policies. Additionally, some policies have percentage-based deductibles for hurricanes. For instance, a 2% deductible on a $300,000 home means you’d pay $6,000 out-of-pocket before coverage kicks in. Review your policy annually to ensure it addresses the risks specific to your area and reflects current replacement costs.</p>

</div>

</div>

<div class="accordion-item">

<div class="accordion-header">

<span>How much cash should I keep on hand for emergencies?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>Keep enough cash to cover one to two weeks of essential expenses, such as food, fuel, and lodging. Use smaller denominations ($1, $5, $10, $20) and store them in a secure, waterproof container. This ensures you’re prepared if power outages make ATMs or card systems unusable. Avoid keeping large sums at home for security reasons, but make sure you have enough for immediate post-disaster needs.</p>

</div>

</div>

<div class="accordion-item">

<div class="accordion-header">

<span>How often should I update my financial disaster preparedness plan?</span>

<div class="accordion-icon"></div>

</div>

<div class="accordion-content">

<p>At a minimum, review your plan annually - though quarterly updates are even better. Tie these reviews to key dates like tax season or insurance renewals. Additionally, update your plan after major life changes, such as moving, marriage, divorce, having a child, or changing jobs. Regular updates ensure your emergency fund, insurance coverage, and document backups stay aligned with your evolving needs.</p>

</div>

</div>

</div>