Bank sweep networks represent a sophisticated solution for individuals and businesses with substantial cash deposits who need FDIC insurance coverage beyond the standard $250,000 limit. These networks automatically distribute your funds across multiple FDIC-insured banks, ensuring every dollar receives full government protection while maintaining the convenience of a single account relationship.

Understanding Bank Sweep Networks and FDIC Insurance Limits

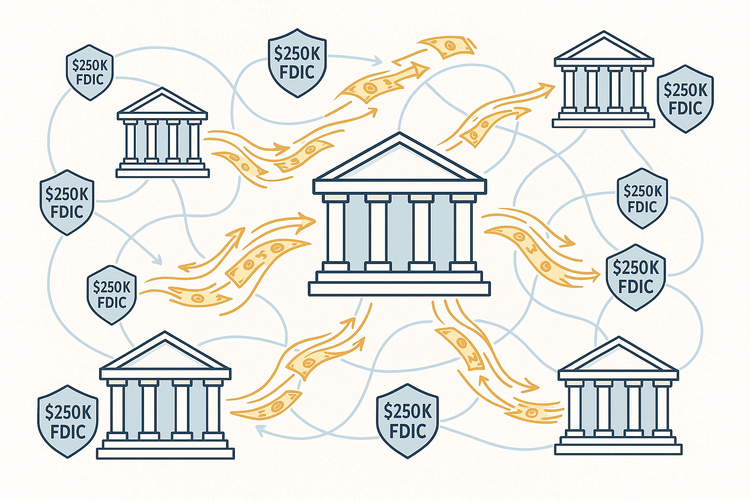

The standard FDIC insurance protects $250,000 per depositor, per bank, per ownership category. That's great for most folks, but what if you've got millions sitting around?

Bank sweep networks solve this problem by automatically spreading your deposits across multiple FDIC-insured banks. Think of it like having dozens of bank accounts without the paperwork headache.

Here's a real example: You deposit $5 million into a sweep network. The system automatically splits this across 20 different banks at $250,000 each. Every single dollar gets FDIC protection.

There are two main types of sweep networks. Reciprocal deposit programs let banks exchange deposits with each other. One-way purchase programs place your money directly into other banks' CDs or deposit accounts.

The FDIC and state banking authorities keep a close eye on these networks. They're legit and regulated—not some sketchy workaround.

How Automatic Fund Distribution Works

Bank sweep networks use sophisticated technology to move your money automatically. The system tracks your total deposits and spreads them across multiple FDIC-insured banks in real-time.

Here's how it works step-by-step. You deposit money into your main account at a participating bank. The sweep network's computer system immediately calculates how much coverage you need. It then distributes your funds across dozens of partner banks, keeping each deposit under $250,000 per institution.

Daily Operations and Settlement

Every business day, the network performs automatic sweeps. Your money moves between banks based on deposits, withdrawals, and interest payments. The technology ensures you never exceed FDIC limits at any single institution.

For example, if you deposit $2 million, the system might place $250,000 each across eight different banks. If you withdraw $100,000, it pulls proportionally from multiple institutions to maintain optimal coverage.

Technology Systems and Tracking

Modern sweep networks use cloud-based platforms that update balances in real-time. You'll see one consolidated statement showing your total balance, even though your money sits in multiple banks. The system tracks interest rates, bank ratings, and regulatory changes automatically.

Most networks provide online dashboards where you can monitor your fund distribution. You can see exactly which banks hold your money and how much FDIC coverage you have. Some platforms even send alerts if your deposits approach coverage limits.

Consolidated Reporting Features

Instead of receiving dozens of bank statements, you get one comprehensive report. This simplifies tax preparation and accounting. The network handles all the paperwork with individual banks, so you don't need to manage multiple relationships.

Many sweep networks integrate with popular accounting software like QuickBooks. This makes it easy for businesses to track cash flow and reconcile accounts. For individuals, the consolidated reporting works well with personal finance tracking tools like Monefy.

The settlement process happens behind the scenes through the Federal Reserve system. Your deposits are fully protected during transfers, and you maintain complete liquidity throughout the process.

Coverage Limits and Calculation Methods

Bank sweep networks typically offer FDIC coverage ranging from $12.5 million to $150 million per depositor. The exact amount depends on the network size and participating banks.

Each bank in the network provides the standard $250,000 FDIC insurance per depositor. So a network with 200 banks could theoretically protect up to $50 million for one person. Networks with 600 participating banks can protect $150 million.

Your ownership category affects total coverage significantly. Individual accounts, joint accounts, trust accounts, and business accounts each get separate $250,000 coverage at every bank. A married couple with individual and joint accounts could get $750,000 coverage per bank ($250k individual + $250k individual + $250k joint).

Here's how the math works: If you have $10 million in individual funds, the network spreads $250,000 across 40 different banks. Each deposit gets full FDIC protection. Your money stays liquid while maximizing insurance coverage.

Coverage calculation example:

- Individual account: $250,000 × 200 banks = $50 million

- Joint account: $250,000 × 200 banks = $50 million

- Trust account: $250,000 × 200 banks = $50 million

- Total potential coverage: $150 million

Network size matters for maximum protection. Smaller networks with 50 banks limit you to $12.5 million in individual coverage. Larger networks provide more flexibility for high-net-worth clients.

Some networks exclude certain bank types or have geographic restrictions. Credit unions and savings associations might not participate in every network. Always verify the actual participating institution count before depositing large amounts.

For businesses, the calculation gets more complex. Different business structures (LLC, corporation, partnership) each qualify for separate coverage. A business owner could potentially get coverage for personal accounts, business accounts, and retirement accounts across the same network.

Consider using banking comparison tools to evaluate different sweep network options and their coverage limits. The platform helps you compare features and find the best fit for your deposit amount.

Who Benefits Most from Bank Sweep Networks

Bank sweep networks aren't for everyone. You need serious cash to make the fees worth it.

Most providers require at least $250,000 to get started. Some want $1 million or more. That puts these services squarely in wealthy territory.

High-Net-Worth Individuals

Rich folks love sweep networks for obvious reasons. If you've got $2 million sitting in checking accounts, you're only protected up to $250,000. That leaves $1.75 million completely exposed.

Retirees often fall into this category. They might have sold a business or inherited money. Suddenly they're sitting on huge cash piles with nowhere safe to put them.

Business owners after exits face the same problem. You sell your company for $10 million and need somewhere to park the cash while you figure out your next move.

Many wealthy individuals prefer keeping 6-12 months of expenses in liquid, FDIC-insured accounts regardless of their investment portfolio size. This conservative approach ensures they won't need to sell investments during market downturns to cover unexpected expenses.

For those seeking higher returns while maintaining FDIC protection, combining sweep networks with high-yield savings strategies can optimize their cash management approach. Some investors use sweep networks as a temporary holding strategy before making larger investment decisions through platforms for diversified portfolio building.

Estate Planning and Trust Applications

Wealthy families often use sweep networks within trust structures to maximize FDIC coverage across multiple beneficiaries. Each trust can qualify for separate FDIC insurance limits, potentially multiplying total coverage significantly.

This strategy works particularly well for families managing generational wealth transfers. Parents can establish multiple trusts for children and grandchildren, each with its own sweep network coverage, ensuring family assets remain protected during estate transitions.

Businesses with Large Cash Reserves

Companies use sweep networks more than individuals. Here's why it makes sense:

Seasonal businesses see huge cash swings. A ski resort might collect $5 million during winter season. They need that money protected but accessible for summer operations.

Professional service firms hold client funds regularly. Law firms managing settlement money or real estate agencies handling earnest money deposits can't afford to lose a penny.

Construction companies often maintain large project accounts. A $20 million development project needs serious cash management throughout the build.

Seasonal businesses benefit most from bank sweep networks during cash flow peaks. Construction companies often hold millions during busy summer months before winter slowdowns. Retail businesses accumulate cash before holiday seasons, then spend it on inventory and operations.

Companies preparing for major acquisitions need secure places to park large sums. A tech startup raising $10 million can't risk losing funds if their primary bank fails. Sweep networks protect these critical funds while maintaining instant access for deal closures.

Manufacturing firms with large payroll obligations use sweep networks for workforce security. A factory with 500 employees needs $2-3 million monthly for wages and benefits. Business financing options can complement sweep networks for companies managing both deposits and credit needs.

Real estate developers managing project funds face unique challenges. They might hold $50 million from investors for 18 months before construction begins. Traditional banks can't protect these amounts, making sweep networks essential for fiduciary responsibility.

Professional Service Firms and Client Funds

Law firms handling class action settlements or estate distributions need maximum FDIC protection. A single case might generate $25 million in client funds requiring secure management. Legal ethics require protecting client money, making sweep networks a professional necessity.

Real estate agencies managing earnest money and closing funds use sweep networks during market booms. When home sales surge, agencies might hold $5-10 million in escrow accounts. Each transaction needs protection until closing completes.

Accounting firms managing tax refunds and business proceeds rely on sweep networks during tax season. CPA firms often hold millions in client funds between February and April. Business accounts offer additional international capabilities for firms with global clients.

Investment advisors use sweep networks as cash management tools for high-net-worth clients. Before deploying funds into markets, advisors park large sums in sweep networks. This provides safety during market volatility while maintaining liquidity for opportunities.

Municipal Governments and Institutions

Government entities love sweep networks. They're handling taxpayer money and can't take risks.

School districts, city governments, and state agencies often have millions in operating funds. They need every dollar protected while maintaining liquidity for payroll and expenses.

Non-profits managing large endowments or major donations also benefit. A hospital foundation receiving a $5 million gift needs immediate FDIC protection while planning how to invest long-term.

When Sweep Networks Don't Make Sense

Skip sweep networks if you've got under $500,000. The fees will eat into your returns too much.

Young entrepreneurs building wealth should focus on investment platforms with lowest fees instead. Your money will grow faster in diversified portfolios than sitting in cash.

If you're comfortable with some risk, high-yield savings accounts or money market funds might offer better returns without the sweep network fees.

The sweet spot for sweep networks? You've got $1 million+ in cash, need it liquid, and want zero risk of loss. That's a pretty specific situation, but for those who fit it, sweep networks are perfect.

Costs, Fees, and Service Comparison

Bank sweep networks charge annual management fees that typically range from 0.25% to 0.75% of your total deposits. For a $5 million deposit, you'd pay between $12,500 and $37,500 per year for the service.

The fee structure varies significantly among providers. IntraFi charges around 0.30% to 0.50% annually for most accounts. Yankee Sweep typically runs 0.35% to 0.60% depending on deposit size. MaxSafe often starts at 0.50% but may negotiate lower rates for deposits exceeding $10 million.

Here's what you can expect across major providers:

| Provider | Annual Fee Range | Minimum Deposit | Maximum Coverage |

|---|---|---|---|

| IntraFi | 0.30% - 0.50% | $250,000 | $150 million |

| Yankee Sweep | 0.35% - 0.60% | $500,000 | $100 million |

| MaxSafe | 0.50% - 0.75% | $1 million | $250 million |

Hidden Costs and Rate Considerations

Beyond management fees, sweep networks often offer lower interest rates than you'd get with direct high-yield savings accounts. While a top online bank might pay 5.3% APY, sweep networks typically offer 4.5% to 5.0% on the same deposits.

This rate difference acts as an additional hidden cost. On a $5 million deposit, a 0.5% rate difference costs you $25,000 annually in lost interest—on top of management fees.

Some networks also charge setup fees ranging from $500 to $2,500. Wire transfer fees for large deposits can add another $25 to $50 per transaction. Monthly statement fees might run $10 to $25 if you prefer paper statements.

Bank sweep networks typically offer competitive interest rates that track closely with current Federal Reserve rates and market conditions. Most sweep networks pay between 4.5% to 5.2% APY, depending on current Federal Reserve rates and network policies.

The trade-off is clear: you're sacrificing some earning potential for maximum FDIC protection. A high-yield savings account might pay 5.3% APY, while your sweep network offers 4.8% APY. On a $5 million deposit, that's a difference of $25,000 per year in interest income.

However, sweep networks become more attractive during rising rate environments. Federal Reserve rate increases typically flow through to sweep network yields within 30-60 days. Some networks also offer tiered rates, paying higher yields on larger balances.

Break-Even Analysis for Different Amounts

The math works differently depending on your deposit size. For deposits under $1 million, you might be better off splitting funds manually across multiple banks. The break-even point usually sits around $2 million, where the convenience justifies the costs.

Consider a $10 million deposit scenario. Manual management across 40 banks would require significant time and tracking. A sweep network charging 0.50% ($50,000 annually) becomes cost-effective compared to hiring staff or spending dozens of hours monthly on account management.

Fee Negotiation Strategies

Large depositors often negotiate better rates. Deposits exceeding $25 million frequently secure fees below 0.30%. Some providers waive setup fees for deposits over $10 million.

Your existing bank relationships matter too. If you're already a private banking client, your institution might offer preferential sweep network pricing. Business account holders often receive volume discounts across multiple services.

Consider bundling sweep services with other products. Some banks reduce sweep fees if you also use their lending, investment, or treasury management services. This bundling approach can cut total costs by 0.10% to 0.25% annually.

Smart depositors use multiple strategies to optimize their returns while maintaining full FDIC coverage. You can combine sweep networks with direct bank relationships, spreading funds across different ownership categories to increase total coverage.

Consider splitting large deposits between sweep networks and high-yield savings accounts at top-paying banks. Keep your most liquid funds (emergency reserves, operating cash) in sweep networks for convenience and safety. Place longer-term savings in direct bank relationships or CD accounts for better rates.

Some wealthy individuals also use multiple sweep networks to exceed single-network limits. IntraFi might cover $150 million while Yankee Sweep covers another $100 million, giving you $250 million in total FDIC protection across both networks.

Large depositors often negotiate better rates with their relationship banks. If you're bringing $10+ million to a sweep network, ask about premium rate tiers or fee reductions. Many banks will waive management fees or offer rate bonuses to secure large deposits.

Timing also matters for rate optimization. Consider moving funds into sweep networks during uncertain market periods, then shifting to higher-yield options during stable times. This strategy works well for businesses with seasonal cash flows or individuals managing large liquidity events.

How to Access Bank Sweep Networks

Getting started with bank sweep networks isn't as complicated as it sounds. You've got three main paths to access these services.

The biggest players in the game are IntraFi (which used to be called CDARS and ICS), American Deposit Management, and MaxSafe. These companies run the networks that connect hundreds of banks across the country.

Finding the Right Bank Partner

Most major banks and credit unions offer sweep network services. You don't go directly to IntraFi or the other network providers—you work through a participating bank.

Banks like Wells Fargo, Bank of America, and many regional institutions offer these services. Credit unions are often great options too since they typically charge lower fees.

Here's the catch: minimum deposits usually start at $250,000. Some banks require $1 million to get started. That's because the whole point is spreading money across multiple banks to beat the $250,000 FDIC limit.

The Application Process

Setting up a sweep account takes about 2-4 weeks from start to finish. You'll need standard banking documents—ID, Social Security number, proof of address, and source of funds documentation.

For businesses, expect to provide:

- Articles of incorporation

- Operating agreements

- Tax ID numbers

- Board resolutions authorizing the account

The bank will also run background checks and verify your identity through their standard procedures.

Choosing Between Network Types

You've got two main options: reciprocal deposits and one-way purchase programs.

Reciprocal deposits work like a swap meet. Your bank sends your excess deposits to other banks in the network, and those banks send their excess deposits back to your bank. Everyone stays balanced.

One-way purchase programs are simpler. Your bank just places your money in other network banks without any swapping involved.

Most people go with reciprocal deposits because they tend to offer better rates and more flexibility.

Questions to Ask Before You Sign Up

Don't just pick the first bank that offers sweep services. Ask these key questions:

- What's the annual fee structure?

- How many banks are in their network?

- What's the geographic spread of those banks?

- How quickly can you access your money?

- What kind of reporting do they provide?

Also check if they offer online access to track where your money is placed. Some banks still mail paper statements, which is pretty outdated for managing millions in deposits.

Setting Up Your Account Structure

Think about how you want to structure ownership before you apply. Different ownership categories get separate FDIC coverage.

For example, you could have individual accounts, joint accounts with your spouse, trust accounts, and business accounts—all with separate $250,000 coverage at each bank in the network.

This is where things get interesting for wealthy families. You might be able to get $150 million or more in total coverage by structuring accounts correctly across multiple ownership types.

Integration with Your Banking Setup

Most people keep their primary checking account at their main bank and use the sweep network for excess cash storage. You can usually transfer money between your regular account and the sweep network pretty easily.

Some banks offer automatic sweeping—any balance over a certain amount in your checking account automatically moves to the sweep network. Others require manual transfers.

For businesses, you'll want to make sure the sweep account integrates with your accounting software. Most major platforms like QuickBooks can handle the consolidated reporting that sweep networks provide.

If you're looking for high-yield savings options to compare against sweep networks, it's worth exploring what rates you can get with simpler products first.

The setup process might seem like a lot of work, but once you're in, managing millions in FDIC-insured deposits becomes pretty straightforward. Just remember—you're paying for convenience and safety, not maximum returns.

Choosing the Right Provider and Institution

Finding the best sweep network provider requires careful research and comparison. Start by evaluating the network size and geographic distribution of participating banks. Larger networks offer better diversification but may charge higher fees.

Key Questions to Ask Potential Partners

Ask about minimum deposit requirements, which typically range from $250,000 to $1 million. Find out how quickly you can access your funds and whether there are any withdrawal restrictions. Most sweep networks offer same-day liquidity, but confirm this before signing up.

Request details about their technology platform and reporting capabilities. You'll want consolidated statements that show all your deposits across the network. Some providers offer real-time online access while others send monthly paper statements.

Due Diligence on Network Quality

Research the credit ratings of banks in the network. Most reputable sweep networks only include well-capitalized institutions with strong regulatory standings. Banking comparison tools can help you evaluate different banking options and their safety ratings.

Check if the provider offers geographic diversification across multiple states. This reduces concentration risk if regional economic problems affect local banks. Some networks focus on community banks while others include larger regional institutions.

Technology and Service Evaluation

Test the provider's online platform and mobile access before committing large deposits. You should be able to view balances, transaction history, and generate reports easily. Poor technology can make managing your sweep account frustrating.

Compare customer service availability and response times. Since you're dealing with substantial amounts, you'll want access to knowledgeable representatives who can handle complex requests quickly. Some providers offer dedicated relationship managers for high-balance clients.

Consider integration capabilities with your existing business banking accounts or wealth management systems. Seamless data transfer can save significant time on accounting and tax preparation.

Implementation Strategy and Best Practices

Setting up bank sweep networks requires careful planning and coordination with your existing financial relationships. Here's how to make the transition smooth and maximize your FDIC coverage.

Planning Your Transition

Start by calculating your exact coverage needs across all account types. Most people underestimate how ownership categories affect their total protection limits.

Review your current banking relationships before making changes. You'll want to maintain some direct bank accounts for day-to-day operations while moving excess funds to sweep networks.

Document everything during the transition process. Keep records of fund movements, fee structures, and network bank listings for tax purposes.

Coordinating with Existing Banks

Contact your primary bank first to discuss sweep network options. Many major banks offer these services but don't actively promote them to smaller depositors.

Ask about integration with your current business accounts or savings accounts. Some banks can seamlessly transfer funds between traditional accounts and sweep networks.

Negotiate fees if you're bringing substantial deposits. Banks often waive or reduce sweep network fees for high-value customers.

For comparison shopping, check platforms to evaluate different institutions' sweep network offerings.

Tax and Accounting Considerations

Sweep networks generate multiple 1099-INT forms since you're technically earning interest from dozens of banks. This creates more paperwork but doesn't change your tax liability.

Set up a dedicated folder for sweep network documentation. You'll receive statements from the managing institution plus individual bank confirmations.

Coordinate with your accountant before implementation. They may recommend timing the transition to align with your tax year or business accounting periods.

Technology Integration and Monitoring

Most sweep networks offer online dashboards showing your fund distribution across member banks. Set up automatic alerts for balance changes and network updates.

Download mobile apps from your sweep network provider for real-time monitoring. You can usually view which banks hold your funds and track interest earnings.

Establish backup access methods in case of technology failures. Keep phone numbers for customer service and know your account numbers at the managing institution.

Exit Strategies and Contingency Planning

Plan your exit strategy before you need it. Understand withdrawal procedures, timing requirements, and any penalties for early termination.

Keep some funds in traditional accounts for immediate access. Sweep networks typically process withdrawals within 1-2 business days, but emergencies don't wait.

Monitor network bank ratings quarterly using FDIC databases. If member banks show financial stress, you may want to reduce your exposure or switch networks.

Create a backup plan for network disruptions. Research alternative sweep providers and maintain relationships with high-yield savings accounts as temporary parking spots for large deposits.

Ongoing Management Best Practices

Review your coverage annually as deposit amounts and family situations change. Marriage, divorce, or business structure changes can affect your optimal FDIC strategy.

Stay informed about network changes. Banks join and leave sweep networks regularly, which can affect your total coverage capacity.

Track performance against alternatives like robo-advisors or low-fee investment platforms to ensure sweep networks still make sense for your situation.

Set calendar reminders to reassess your strategy every six months. Interest rate environments change, and better options may become available.

Bank sweep networks offer an elegant solution for managing substantial cash deposits while maintaining full FDIC protection. Though they come with fees and slightly lower interest rates, the convenience and peace of mind they provide make them invaluable for high-net-worth individuals, businesses, and institutions dealing with large liquid assets. By understanding the mechanics, costs, and implementation strategies outlined above, you can make informed decisions about whether sweep networks fit your financial situation and how to optimize their benefits for your specific needs.

Questions? Answers.

Common questions about bank sweep networks

Most bank sweep networks require a minimum deposit of $250,000 to get started, though some providers require $500,000 or even $1 million. This minimum exists because the primary benefit of sweep networks is spreading deposits beyond the standard $250,000 FDIC insurance limit across multiple banks.

Most sweep networks offer same-day or next-business-day access to your funds. While your money is spread across multiple banks, the managing institution can typically process withdrawal requests within 1-2 business days. Some networks offer immediate access up to certain limits, similar to traditional bank accounts.

Yes, sweep networks are fully FDIC insured. Each participating bank in the network provides the standard $250,000 FDIC coverage per depositor. If a network has 200 banks, you could potentially receive up to $50 million in coverage ($250,000 × 200 banks). The FDIC treats each bank relationship separately, ensuring full protection across the entire network.

Annual management fees typically range from 0.25% to 0.75% of your total deposits. For example, on a $5 million deposit, you might pay $12,500 to $37,500 annually. Additional costs may include setup fees ($500-$2,500), wire transfer fees ($25-$50), and potentially lower interest rates compared to high-yield savings accounts. For expense tracking, consider using budgeting apps like Monefy to monitor these costs.

Yes, you can use multiple sweep networks simultaneously to increase total FDIC coverage, as long as they don't share the same participating banks. For example, you might use both IntraFi and Yankee Sweep networks if they have different bank partners. However, you'll need to carefully track which banks participate in each network to avoid overlap that could reduce your effective coverage.